대한 책임을 국가의 국내 총생산 (GDP)의), 그러나 또한 월별 무역 데이터를보고하는 최초의 주요 수출 국가로

발생하기 때문이다. 즉 국제 무역 흐름 완벽하게 기압, 또는 경우에 따라, 국제 무역 탄광의 카나리아. 그것은

또한 우리가 "라고 할 때 우리는 한 일주일 전에보고 무엇을 확인하는 글로벌 무역이 자유 낙하에 ".

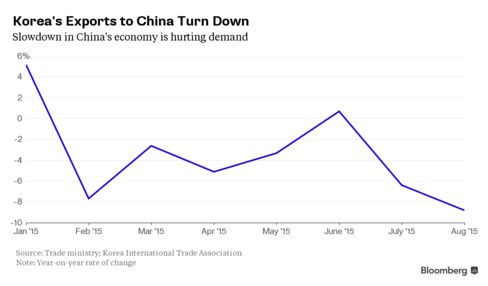

한국어 무역 대학살은 다음과 클레이 차트에 틀림없는 것입니다 :

맥락에서 한국 폭락 무역 퍼팅이 2009 년 8 월 이후 최악의 월간 감소했고, 수입 18.3 % 공중제비 월 이후

가장 큰 하락에 의해 결합되었다. 무역 적자 : 나쁜, 한국은 곧 진정한 블랙 스완으로 실행할 수 있습니다 8 월,

국가의 무역 수지 흑자는 그쪽으로 예상 $ 6.1 억, 7 월 절반은 $ 7.7 billion 흑자 tthan 거의 이하 제 악화

다만 $ 4.3 억 하나에 강화 중국의 환율 전쟁으로 다음 아시아 통화의 평가 절하가 유출 통해 세계 무역의

가장 중요한 선구자가 될 수 있습니다 무엇 : 제안 한국은 옆 매장에 찍어, 또는 마지막으로 늦은 감이 말했다

많은 것을에 참여하도록 강요 할 수있다.

또한, 전체 한국어 수출의 1/4은 이웃 중국으로가는,이 무역 데이터는 중국 경제에 무슨 일이 일어나고 있는지

훨씬 더 정확한 지표이다.

김 두-UN, 서울 하나 대투 증권 이코노미스트는 로이터 통신에 말했다 "중국 경제의 상태는 한국의 수출에 매우

중요하지만, 우리가 의미있는 개선이 표시되지 않습니다 : 중국의 경제가 회복 관리하지 않는 한국의 우울한

그림은 개선되지 않습니다 올해 말 전에, "김은 그가 집에서 경제 활동을 촉진하기 위해 2015 년에 의해

한국으로 절단 한 번 더 속도를보고했다. 한국의 현재 정책 금리는 1.50 %를 의미합니다.

우리는, 다른 한편으로는, 중국 최근 실시한 것의 라인을 따라, BOK 의해 훨씬 더 공격적 절하를 예상하고있다.

클레이는 한심한 데이터로 더 깊이 파고 :

자동차 및 선박 출하량은 석유 화학, 광물, 철강에 약한 기본 추세를 악화 및 임시 전자 제품에서 선택 마스킹, 8 월에 급격히 떨어졌다. 자동 출하량은 새로운 발사의 상승 파이프 라인에도 불구하고, 8 월에 32.4 % y / y을 떨어지고, 특히 실망했다. 선박 배송은 7 월 한 달 서지 (+ 56.7 %)을 다시 지불, 8 월에 큰 폭 (-24.5 %)을 떨어졌다. 선박 및 자동차는 14.7 %의 헤드 라인 가을의 4.3pp을 만들어 결합했다. 우리는 석유 화학, 광물, 철강을 포함하는 경우, 헤드 라인 가을의 거의 11.4pp는 설명 될 수있다. 8 월 한 실버 라이닝은 하락 속, 전자 출하량은 바닥을 할 수있다 징후가있는 것이 었습니다. 모바일 기기와 PC의 수출 7 월에 감소 후, 각각 14.5 %와 8.6 %를 증가했다. 가전 출하량 드래그도 좁아. (+ 6.2 %, 6 월 7 월 2.9 %) 반도체는 5.7 % 증가하는 데 성공했습니다. CNY가 평가 절하 된 후 불길, 중국, 한국의 가장 큰 무역 파트너 출하량은 7.6 % 하락, 7 월의 6.4 % 하락을 확장 가능성 단말기 및 자동차의 속도가 느린 판매 때문에, 감소 중국어 구매력을 반영, 8 월에 더 큰 폭 하락 8월 11일 후.

거의 모든 제품 cateogries에서 드롭을 보여주는 또 다른 고장은 골드만에서 YY 차트의 호의를 제공 :

다음과 같은 약점의 지리적 분포했다 : 미국 선적 (+ 3.4 %)는 소폭 더 했더라도 유럽 (-7.7 %),

일본 (-20.9 %)과 아세안 (-3 %) 물량은 8 월에 부진.

이것은 명백한 제외하고, 세계 경제에 대해 무엇을 의미 하는가 :

우리의 관심은 7 월에 1.29x에 재고 / 출하 비율 점프 함께 (6 월 : 1.29x, 4 ~ 5 월 : 1.27 배 3 월 : 1.24), 2008 년 12 월에 그것을 글로벌 금융 위기 기록 아래 그늘 잎 . (1.30x) 높은 재고를 모두 공급 체인은, 앞서 개월 IP에 약한 하위 50 일경 PMI 수치에 의해 강조 포인트 무게 가능성이있다 (8 월 : 47.9을 7 월 : 47.6)

이 놀라운 여기에 한국의 통화 정책에 대한 의미 무엇에 관해서는 자세한 완화.

우리는 지금 한국 은행이 추가로 25bp에 속도가 10 월에 가장 가능성, 4 분기에 잘라 제공 할 것으로 예상된다. 우리는 9 월 11 일 회의에서, 이전 움직임의 외부 기회를 볼 수 있지만, 우리는 한국 은행이 재정 보조 지출의 초기 배달 17-18 9 월 미국 FOMC 회의 후 이동하는 것을 선호 것이라고 생각하는 것을 계속한다. 또한, 우리는 지금 3 분기 (16)에 국내 최초의 금리 인상을 기대하기보다는 건강한 포스트 MERS 반등을 보여주는 서비스 경제의 주요 지표와 또한 후반 1 분기 (16)에, 우리는 즉시 행동 할 수있는 긴급 여전히 낮은 믿습니다. 아마도 연료 필수 상품을 비축하여 - - 남아 우리는 약한 원 바이어스 엔지니어링의 기존 초점 생각합니다.

물론, 더 한국, 또는 크게 평가 절하에 의해 완화, 볼이 다음 다음 자신의 추가 완화 (또는 평가 절하)와 한국의

이동과 일치하도록 강요됩니다 한국의 무역 경쟁, 법원에 의미, 등, 때까지 하나는 더 이상 양탄자에서 글로벌

경기 침체를 청소 할 수 없습니다. 그것은 아무것도 아래로 글로벌 경쟁 호출되지 않습니다.

우리가 빈정 지난 해에 대한 주석왔다으로, 글로벌 중앙 은행이 무역을 인쇄 할 수 배웠 더라면 확실히,이 모든

피할 수 있었다.

지금 그러나, 우리는 앉아서 한국이 글로벌 통화 평가 절하의 악 대차 가입 최신 국가를수록 기다립니다.

우리는 기다릴 오래가 없습니다.

Global Trade In Freefall: South Korea Exports Crash Most Since 2009

While the market's attention overnight was focused on China's crumbling manufacturing and service PMI, data which was already hinted in the flash PMI reports earlier in August, the real stunner came not from China but from South Korea, which last night reported an unprecedented 14.7% collapse in exports, far worse than the -5.9% consensus estimate, and more than 4 times worse than July's 3.4%.

The number is critical because not only do exports account for about half of South Korea's GDP (with Samusng alone anecdotally accountable for 20% of the country's GDP), but because it also happens to be the first major exporting country to report monthly trade data. That makes it the perfect barometer of global trade flows, or as the case may be, the canary in the global trade coalmine. It also confirms what we reported just one week ago when we said that "Global Trade Is In Freefall".

The carnage in Korean trade is unmistakable in the following Barclays chart:

Putting South Korea plunging trade in context, this was the worst monthly decline since August 2009, and was coupled by an 18.3% tumble in imports, the biggest drop since February. Worse, South Korea may soon run into a true Black Swan: a trade deficit: in August, the country's trade surplus tightened to just $4.3 billion, one third worse than tha $6.1 billion expected, and nearly less tthan half the $7.7 billion surplus in July, suggesting South Korea may be forced to dip into its reserves next, or finally engage in what many have said is long overdue: the next Asian currency devaluation as China's FX war spills over to what may be the most important harbinger of global trade.

Furthermore, with one quarter of total Korean exports going to neighbor China, this trade data is a far more accurate indicator of what is happening in China's economy.

Kim Doo-un, economist at Hana Daetoo Securities in Seoul, told Reuters that Korea's gloomy picture will not improve unless China's economy manages to rebound: "The state of the Chinese economy is crucial to South Korean exports but we will not see meaningful improvement there before the end of this year," Kim added he sees one more rate cut in South Korea by end-2015 to boost economic activity at home. South Korea's current policy rate stands at 1.50 percent.

We, on the other hand, anticipate far more aggressive devaluation by the BOK, along the lines of what China recently conducted.

Barclays digs deeper into the abysmal data:

Autos and vessel shipments fell sharply in August, exacerbating the weak underlying trend in petrochemicals, minerals and steel and masking a tentative pick up in electronics. Auto shipments were particularly disappointing, falling 32.4% y/y in August, despite a rising pipeline of new launches. Vessel deliveries also dropped sharply (-24.5%) in August, paying back the one-month surge (+56.7%) in July. Vessels and autos combined made up 4.3pp of the 14.7% headline fall. If we include petrochemicals, minerals and steel, almost 11.4pp of headline fall can be explained. One silver lining in August was that amid the declines, there are signs that electronics shipments may be bottoming out. Exports of mobile devices and PCs jumped 14.5% and 8.6%, respectively, after declining in July. The drag in household electronics shipments also narrowed. Semiconductors, managed to grow 5.7% (July: +6.2%; June: 2.9%). Ominously, shipments to China, Korea’s largest trading partner, fell more sharply in August, falling 7.6% and extending the 6.4% drop in July, likely owing to slower sales of handsets and autos, and reflecting reduced Chinese purchasing power after the CNY was devalued after 11 August.

Another breakdown showing the drop across virtually all product cateogries comes courtesy of the Y-Y chart from Goldman:

The geographic distribution of the weakness was as follows: shipments to Europe (-7.7%), Japan (-20.9%) and ASEAN (-3%) also remained sluggish in August, although US shipments (+3.4%) did marginally better.

What does this mean for the global economy, aside from the obvious:

Our concern is with the jump in the inventory/shipment ratio to 1.29x in July (June: 1.29x; April-May: 1.27x; March: 1.24x), which leaves it a shade below the Global Financial Crisis record in December 2008 (1.30x). High inventories in both supply chains are likely to weigh on IP in the months ahead, a point underscored by the weak sub-50 Nikkei PMI readings (August: 47.9; July: 47.6)

As for what this means for Korean monetary policy, no surprise here: more easing.

We now expect the BoK to deliver a further 25bp rate cut in Q4, most likely in October. We see an outside chance of an earlier move, at the 11 September meeting, but we continue to believe that the BoK will prefer to move after the initial delivery of the fiscal supplementary spending and the US FOMC meeting on 17-18 September. Also, we now expect the first rate hike in Korea in Q3 16, rather than in late Q1 16. Moreover, with key indicators for the services economy showing a healthy post-MERS rebound, we believe the urgency to act immediately is still low. We believe the existing focus on engineering a weaker KRW bias – possibly by stockpiling essential commodities such as fuel – will remain.

Of course, further easing by South Korea, or even an outright devaluation, means the ball will then be in the court of Korea's trade competitors, who will then be compelled to match the Korean move with further easing (or devaluation) of their own, and so on, until one can no longer sweep the global recession under the rug. It isn't called the global race to the bottom for nothing.

To be sure, all of this could have been avoided if as we have sarcastically been commenting for the past year, global central banks had learned to print trade.

For now however, we sit back and wait as South Korea becomes the latest country to join the global currency devaluation bandwagon. We won't have long to wait.

@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

한국 수출은 15 % --- 중국 디플레이션이 빠르게 확산 플 런지

한국 - 중국 세계 최대의 수출국 - 그것의 더 큰 이웃이 2009 가장을 쏟아 출하량을 보내 도움에서

수요 감소로 압박 받고있다.

모든 주요 시장에 출하 하락으로 미국의 수출은 무역 사역에 따르면, 전년 대비 8 월 여덟째 개월 연속

감소 14.7 %로 하락했다. 이코노미스트들은 5.9 % 하락을 예상했다.

"당당한 수출이 나쁜 것으로 예상하지만, 데이터가 더 나쁜 것으로 판명되었다,"그것을 리는 한국의

수출의 가장 큰 몫을 복용 재, 중국과 유진 투자 증권 (주) "에 대한 서울 기반 경제를 노래했다 중국의

경제가 개선되지 않는 한 회복을 기대하기는 어려울 것이다. "

슬럼프는 해외 제품을 출시하여 국내 총생산 (GDP)의 절반에 대해 발생하는 국가의 성장에 위험을

제기한다. 바클레이 PLC와 호주 및 뉴질랜드 뱅킹 그룹 (주) 경제학자들은 더 올해 기준 금리를 낮출

것이다 중앙 은행을 예측, 데이터 후 한국의 정책의 은행에 대한 자신의 전화를 변경.

중국어 제조 업체 휴대 전화 부품, 자동차 부품 등 중간재의 공급 업체로서, 한국의 가장 큰 수출 시장의

수요를 약화에서 압력을 받고있다. 중국의 공식 공장 게이지는 3 년 만에 가장 낮은 독서에 8 월에 떨어졌다.

환율 상승

수출도 달러에 대한 원화의 7 % 감가 상각 지금까지이 년 후에 떨어졌다.한국은 위안화 약세에 가장

노출 된 국가 중 하나이며, 국제 금융 연구소의 지난 주에 따라, 부가 가치 체인을 이동하는 중국

기업의 경쟁 증가에 직면하고있다.

일본과 유럽 연합 (EU)에 사람들은 무역 사역에 따라, 각각 24.4 %와 20.8 %로 하락하면서 중국 수송,

전년 대비 8 월에 8.8 % 하락했다. 중국이 약 해졌다에서 중국에 판매 인해 수입 수요 천진 지역에서

폭발과 같이 악화, 문이 보였다.

중국은 S & T 평가 및 계획의 연구원에 따르면, 기술 한국의 우위를 축소된다. 한국 경제에 걸쳐 120 가지

주요 영역에서의 기술 수준은 2012 년 1.9 년 앞서 중국했지만, 2014 년 1.4 년으로 감소했다, 그것은

말했다. 중국어 휴대폰 업체 샤오 미 테크 코리아와 화웨이 기술 유한 회사는 점점 더 그 이익

6 월 종료 기간에서 다섯 번째 분기에 하락 한국의 삼성 전자와 경쟁하고있다.

증가 경쟁

한국 은행은 재무부가 3.1 % 확장 프로젝트 동안 아시아에서 네 번째로 큰 경제가 2.8 %로 올해를

확대 할 것으로 전망. 블룸버그 8월 13일부터 19일까지에 의해 조사 된 경제학자들은 경제가 단지

2.6 % 성장 관리를 참조하십시오.

당국은 또한 네 금리 1.5 %의 전례없는 낮은 8 월부터 인하 작년과 올해 기록 크기의 예산으로, 국내

수요를 촉진하기 위해 노력했다. 그럼에도 불구하고, 경제는 4 ~ 6 월 분기에 0.3 % 증가했다.

한국 은행은 10 월 초와 같은 1.25 %로 금리를 인하 할 가능성이있다, 모건 스탠리 이코노미스트

샤론 램과 성 Woen 강 화요일 노트에 썼다. 중국은 지난 10 년 동안의 주요 성장 동력이었던 반면,

지금 한국 경제에 드래그로 돌 수 있었다, 그들은 말했다.

정부는 더 잘 도와 해외 경쟁 원조와 무역 보험 마케팅 한국 기업을 제공 4월과 7 월에 함께 패키지를

넣어.

한국의 해외 물량의 약 25 %가 무역 사역의 자료에 따르면, 올해 상반기에 중국에 갔다. 중국 매출의

68 %가 중간재 있었고, 단지 4 %가 한국 무역 투자 진흥 공사에 따르면, 소비자 제품이었다. 나머지는

주로 자본재했다.

중국 둔화

그 7.4 %의 속도로 전년 대비 5.9 %의 5 ~ %로 느린 중국의 성장은 한국의 수출은 추가로 2.2 % 포인트

하락할 것이라고해야하며, 경제 성장은 현대 리서치 8월 28일 보고서에 따르면, 0.6 점으로 감소 할 것

연구소.

"중국에 중간재를 보내고 좋은 일 동안 성장의 혜택을 한국과 같은 나라는 이제 더 큰 피해를보고있다"고

봉 Geol, 서울 국제 무역 연구소 이코노미스트는 말했다. "한국 기업은보다 소비재, 서비스 산업 중심의

경제에 대한 중국의 산업 구조의 변화에 적응해야합니다."

Korean Exports Plunge 15%——-China Deflation Rapidly Spreading

South Korea — the world’s biggest exporter to China — is getting squeezed as weaker demand from its larger neighbor helped send its shipments tumbling the most since 2009.

The nation’s exports plunged 14.7 percent in August from a year earlier, an eighth straight monthly decline, as shipments to all its major markets fell, according to the trade ministry. Economists had forecast a 5.9 percent drop.

“August exports had been expected to be bad, but the data turned out to be even worse,” said Lee Sang Jae, a Seoul-based economist for Eugene Investment & Securities Co. “With China taking the largest share of Korea’s exports, it will be difficult to expect a recovery unless China’s economy improves.”

The slump is raising risks to growth in a nation that generates about half of its gross domestic product by shipping products overseas. Barclays Plc and Australia & New Zealand Banking Group Ltd. economists changed their calls for the Bank of Korea’s policy after the data, predicting the central bank will lower its key interest rate further this year.

As a supplier of mobile phone components, car parts and other intermediate goods to Chinese manufacturers, Korea is under pressure from weakening demand in its biggest export market. China’s official factory gauge fell in August to the lowest reading in three years.

Won Depreciation

Exports have fallen even after the won’s 7 percent depreciation against the dollar so far this year. Korea is one of the most exposed nations to weakness in the yuan, and is facing increasing competition from Chinese companies that are moving up the value-added chain, according to the Institute of International Finance last week.

Shipments to China fell 8.8 percent in August from a year earlier, while those to Japan and the European Union fell 24.4 percent and 20.8 percent, respectively, according to the trade ministry. Sales to China deteriorated due to the explosion in Tianjin area and as import demand from China waned, the statement showed.

China is narrowing South Korea’s lead in technology, according to the Korea Institute of S&T Evaluation and Planning. The level of technology in 120 key areas across the Korean economy was 1.9 years ahead of China in 2012, but shrank to 1.4 years in 2014, it said. Chinese handset producers Xiaomi Corp. and Huawei Technologies Co. are increasingly competing with Korea’s Samsung Electronics Co., whose profits fell for a fifth quarter in the period ending June.

Increasing Competition

The Bank of Korea forecasts that Asia’s fourth-biggest economy will expand 2.8 percent this year, while the finance ministry projects a 3.1 percent expansion. Economists surveyed by Bloomberg Aug. 13 to 19 see the economy managing just 2.6 percent growth.

Officials have also sought to spur domestic demand, with four interest-rate cuts since August last year to an unprecedented low of 1.5 percent, and a record-sized budget for this year. Even so, the economy grew just 0.3 percent in the April-June quarter.

The BOK is likely to cut its rate to 1.25 percent as early as October, Morgan Stanley economists Sharon Lam and Sung Woen Kang wrote in a note Tuesday. While China had been a major growth driver over the past decade, it could now turn into drag on the Korean economy, they said.

The government put together packages in April and July that offered Korean firms marketing aid and trade insurance to help them better compete overseas.

About 25 percent of Korea’s overseas shipments went to China in the first half of this year, according to trade ministry data. Of the sales to China, 68 percent were intermediary goods, and only 4 percent were consumer products, according to the Korea Trade-Investment Promotion Agency. The rest was mainly capital goods.

Slowing China

Should China’s growth slow to between 5 percent to 5.9 percent from its 7.4 percent pace last year, South Korea’s exports would fall a further 2.2 percentage points and its economic growth would be reduced by 0.6 point, according to an Aug. 28 report by Hyundai Research Institute.

“Countries like Korea that send intermediary goods to China and benefited from its growth during the good days are now seeing bigger damage,” said Lee Bong Geol, an economist for Institute for International Trade in Seoul. “Korean companies need to adapt to the shift in China’s industrial structure to a more consumer goods, services industry-focused economy.”

@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

죽음은 시장 곳곳에 확산을 십자가

"죽음의 십자가"패턴도 해외 혼란에서 더 많은 절연이 될 것으로 시장 세그먼트를 감염, 전염병처럼

주식 시장을 통해 확산을 계속합니다.

러셀 2000 지수 암내는 -2.02 % 작은 대문자 주식의 주요 시장 지수 중 최신 피해자가되었다. 지수의

50 일 이동 평균은 FactSet에 따라, 1,224.11에 미끄러 200 일 이동 평균 (MA), 아래 교차 화요일 정오

무역에 1,222.95로 떨어졌다.

작은 캡 주식의 죽음 크로스 '바이러스 숨길 수 없습니다

대부분의 차트 전문가들은 50 일 MA는 200 일 MA 이하 교차 할 때, 단기 하락은 장기 하락 추세로

발전하고 있음을 나타냅니다, 죽음의 십자가를 생각합니다.

러셀 2000의 마지막 죽음의 십자가 지수는 1 년 낮은에 바닥을하기 전에 그 후 3 주 또 다른 7.1 %

하락 9월 22일, 2014 년에 나타났다.

즉 월요일에 S & P MidCap 400 지수 MID, -2.20 %로 나타난 죽음의 십자가를 다음과 같습니다.

Midcap 주식 추적기 월요일에 죽음의 교차 감염

작은 캡 기업은 더 큰 모자 회사보다 국제 시장에 덜 노출을하는 경향이 있으므로 해외 시장에서 약세에서

더 많은 절연이 될 것으로 추정된다. S & P 500의 가장 큰 회사, 애플사 AAPL은 -2.66 % 가져 예를 들어,

가장 큰 시가 총액과 러셀 2000 구성 요소는 Anacor 제약 ANAC은 -1.23 %로, FactSet에 따라, 미국에서

수익의 100 %를 가져옵니다 해외 매출의 약 62 %.

중국의 경제와 주식 시장의 붕괴는 지난 몇 주 동안 미국 시장의 변동성을 촉발 도움이되기 때문에,

러셀 2000은 더 넓은 시장을 상회하고있다.

하나, -2.53 % 차트 다시 8월 11일에서 다우 존스 산업 평균의 DJIA에 출연하면서 대형주 추적기,

S & P 500 지수의 SPX 중, -2.55 %로, 지난 금요일 죽음의 십자가를 생산했다.

많은 사람들이 잘 전보 이동 평균 크로스 오버 정말 약세 신호인지 아닌지 의문을 제기했다. 그러나

2008 년 말에, 시장이 바닥 삼개월하기 전에, 모든 30 다우 주식은 죽음의 십자가를 생산했다.

약세 패턴이 등장하고있는 다른 주목할만한 인덱스 중, 다우 존스 전체 주식 시장 지수 DWCF은 -2.50 %도

화요일에 죽음의 십자가를 생산, 다우 존스 운송 평균 DJT은 -1.57 % 월 (26)과 다우에 하나를 생산

존스 유틸리티 평균 DJU은 -2.07 %로 5 월 7 일 하나를 생산했다.

나스닥 종합 2-3주에 대한, 여전히 안전

한편, 나스닥 종합 COMP는 -2.41 %가 2 ~ 삼주 떨어져 죽음의 십자가를 생산에서입니다. 시장의 투매가 어떤 악화 경우는, 많은 빨리 일어날 수 있습니다.

Death Crosses Spread To All Corners Of The Market

“Death cross” patterns continue to spread through the stock market like an epidemic, even infecting market segments believed to be more insulated from overseas turmoil.

The Russell 2000 index RUT, -2.02% of small-capitalization stocks became the latest victim among the major market indexes. The index’s 50-day moving average fell to 1,222.95 in midday trade Tuesday, crossing below the 200-day moving average (MA), which slipped to 1,224.11, according to FactSet.

Small-cap stocks can’t hide from the ‘death cross’ virus

Many chart watchers believe a death cross, when the 50-day MA crosses below the 200-day MA, indicates that a shorter-term decline has developed into a longer-term downtrend.

The Russell 2000’s last death cross appeared on Sept. 22, 2014. The index fell another 7.1% in the three weeks after that before bottoming at a one-year low.

That follows the death cross that appeared in the S&P MidCap 400 Index MID, -2.20% on Monday.

Midcap stocks tracker infected with death cross on Monday

Smaller-cap companies tend to have less exposure to international markets than larger-cap companies, so are believed to be more insulated from weakness in overseas markets. For example, the Russell 2000 component with the largest market cap, Anacor Pharmaceuticals ANAC, -1.23% gets 100% of its revenue from the U.S., according to FactSet, while the S&P 500’s largest company, Apple Inc. AAPL, -2.66% gets about 62% of its revenue from overseas.

Since the meltdown in China’s economy and stock market helped spark the volatility in U.S. markets in the last few weeks, the Russell 2000 has outperformed the broader market.

Among the large-cap trackers, the S&P 500 index SPX, -2.55% produced a death cross last Friday, while one appeared in the Dow Jones Industrial Average’s DJIA, -2.53% chart back on Aug. 11.

Many have questioned whether a well-telegraphed moving average crossover is really a bearish signal or not. But at the end of 2008, three months before the market bottomed, all 30 Dow stocks had produced death crosses.

Among other notable indexes in which the bearish pattern has appeared, the Dow Jones Total Stock Market Index DWCF, -2.50% also produced a death cross on Tuesday, the Dow Jones Transportation Average DJT, -1.57% produced one on May 26 and the Dow Jones Utility Average DJU, -2.07% produced one on May 7.

Nasdaq Composite still safe, for 2-3 weeks

Meanwhile, the Nasdaq Composite COMP, -2.41% is two-to-three weeks away from producing a death cross. It could happen a lot sooner, if the market’s selloff gets any worse.

@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

죽음의 십자가'패턴은 주식 시장의 모든 구석으로 확산

"죽음의 십자가"패턴도 해외 혼란에서 더 많은 절연이 될 것으로 시장 세그먼트를 감염,

전염병처럼 주식 시장을 통해 확산을 계속합니다.

러셀 2000 지수 암내는 -2.71 % 작은 대문자 주식의 주요 시장 지수 중 최신 피해자가

되었다. 지수의 50 일 이동 평균은 FactSet에 따라, 1,224.11에 미끄러 200 일 이동

평균 (MA), 아래 교차 화요일 정오 무역에 1,222.95로 떨어졌다.

작은 캡 주식의 죽음 크로스 '바이러스 숨길 수 없습니다

대부분의 차트 전문가들은 50 일 MA는 200 일 MA 이하 교차 할 때, 단기 하락은

장기 하락 추세로 발전하고 있음을 나타냅니다, 죽음의 십자가를 생각합니다.

러셀 2000의 마지막 죽음의 십자가 지수는 1 년 낮은에 바닥을하기 전에 그 후 3 주

또 다른 7.1 % 하락 9월 22일, 2014 년에 나타났다.

즉, S & P MidCap 400 지수에 나타난 죽음의 십자가 다음과 MID, -2.83 % 일을.

Midcap 주식 추적기 월요일에 죽음의 교차 감염

작은 캡 기업은 더 큰 모자 회사보다 국제 시장에 덜 노출을하는 경향이 있으므로

해외 시장에서 약세에서 더 많은 절연이 될 것으로 추정된다. 예를 들어, 가장 큰 시가

총액과 러셀 2000 구성 요소는 Anacor 제약 ANAC은 -1.08 %로 S & P 500의 가장

Death cross’ patterns spread to all corners of the stock market

“Death cross” patterns continue to spread through the stock market like an epidemic, even infecting market segments believed to be more insulated from overseas turmoil.

The Russell 2000 index RUT, -2.71% of small-capitalization stocks became the latest victim among the major market indexes. The index’s 50-day moving average fell to 1,222.95 in midday trade Tuesday, crossing below the 200-day moving average (MA), which slipped to 1,224.11, according to FactSet.

Small-cap stocks can’t hide from the ‘death cross’ virus

Many chart watchers believe a death cross, when the 50-day MA crosses below the 200-day MA, indicates that a shorter-term decline has developed into a longer-term downtrend.

The Russell 2000’s last death cross appeared on Sept. 22, 2014. The index fell another 7.1% in the three weeks after that before bottoming at a one-year low.

That follows the death cross that appeared in the S&P MidCap 400 IndexMID, -2.83% on Monday.

Midcap stocks tracker infected with death cross on Monday

Smaller-cap companies tend to have less exposure to international markets than larger-cap companies, so are believed to be more insulated from weakness in overseas markets. For example, the Russell 2000 component with the largest market cap, Anacor Pharmaceuticals ANAC, -1.08% gets 100% of its revenue from the U.S., according to FactSet, while the S&P 500’s largest company, Apple Inc. AAPL, +1.46% gets about 62% of its revenue from overseas.

Since the meltdown in China’s economy and stock market , the Russell 2000 has outperformed the broader market.

Among the large-cap trackers, the S&P 500 index SPX, -2.96% produced a death cross last Friday, while one appeared in the Dow Jones Industrial Average’sDJIA, -2.84% chart .

Many have questioned whether a well-telegraphed moving average crossover is really a bearish signal or not. But at the end of 2008, three months before the market bottomed, all 30 Dow stocks had produced death crosses.

Among other notable indexes in which the bearish pattern has appeared, the Dow Jones Total Stock Market Index DWCF, -2.90% also produced a death cross on Tuesday, the Dow Jones Transportation Average DJT, -2.14% produced one on May 26 and the Dow Jones Utility Average DJU, -2.68% produced one on May 7.

Nasdaq Composite still safe, for 2-3 weeks

Meanwhile, the Nasdaq Composite COMP, -2.94% is two-to-three weeks away from producing a death cross. It could happen a lot sooner, if the market’s selloff gets any worse.

@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

S & P 500에 대한 죽음의 촛불

과거의 실적은 항상 미래의 결과를 신뢰할 수있는 지표가 아닙니다. 그러나,이 경우, 아주 잘

할 수있다. 따라서 당신은 뮤추얼 펀드를 통해 또는 401 (K) 중 하나, 주식 시장 노출이있는 경우,

당신은 확실히이 장기 차트의 노트를 만들고 싶어.

아래 차트와 좋은 살펴보고 클릭하면 확대됩니다. 이 끝나면, 독서를 유지하고 우리는 당신이

무엇을보고 설명 할 것이다 :

위의 일반적인 경향은 긍정적 인 S & P 500 주의 25 년, 월간 차트는 있지만 두, 큰 곰 시장 수정으로

표시됩니다.

첫째, S & P에 450 레벨 근처에 1995 년에 시작하여 구매 모멘텀이 마침내 지쳐 있었고 시장이

롤오버하기 시작한 2000 년 8 개월 동안 1,500 근처에 둥근 상단에 모든 방법을 확장 집회를

확인합니다. 종종, 시장의 꼭대기는 일반 20/20 뒷 궁리에 주목하고이 여기 경우가 곧이었다.

쉽게 우리는 파란색 화살표와 차트를 표시 한, 찾을 수 있도록하기 위해 2000 년 12 월 차트에서

큰, 불쾌한 "죽음의 촛불"참고.

2000 년 12 월에, S & P는 1389의 높은보고, 1254의 낮은 1,320의 최종 가까이. .이 달, 범위는

9.72 %이고, 의미 최종 손실은 4.97 %로,이 심한 그린 뒷 궁리의 이익을 다시 차트에 빨간색

촛불은 분명 트렌드 변화와 황소 시장의 끝을 표시했다. S & P는 2002 년 10 월에 바닥 시간으로

지수는 2002 년 10 월 단지 769의 낮은 2000 년 3 월 1553의 피크에서 총 강하는 단 50 % 이상

이었다 769의 낮은에 떨어졌다.

그 2002 낮은에서, 그러나, 새로운 황소 시장 랠리가 시작되었다. 그것은 단지 5 년 동안 지속하며

S & P는 1546에서 2007 년 11 월에 정점. 다시 한번, 주식 시장이 6-8 달에 형성되었다 상단 둥근

지금은 2008 년 초에 이월 위의 차트에서 중간 파란색 화살표를 찾아주십시오하기 시작했다.

거기 발견 된 2008 년 1 월 월과 큰, 불쾌한 "죽음의 촛불"을 가리키고 있습니다.

2008 년 월에, S & P는., 1472의 1270의 낮은 1378의 최종 가까이 높은 보았다 이 달의 범위가

13.72 %로, 의미 최종 손실은. 6.38 %였다 그냥 12 월에로 2000,이 "죽음의 촛불"가파른,

고통스러운 보정의 황소 시장의 끝과 시작을 표시했다. 2007 년 11 월에 1546의 높은에서, S & P는

56.86 %의 총 드롭의 2009 년 3 월 667의 낮은에 떨어졌다. 아싸!

어떤이 다시 한번 일, 8 월 2015 년의 단지 완료된 달을 가리키는 차트에서 세 번째 파란색 화살표를

제시하는 우리에게 가져다, S & P가 나타납니다은 6-8 달 위반 여러 차례 실패, 상단 둥근

완료하기 뚱뚱한 저항 차트 ... 다른 죽음의 촛불에 그려진 된 내용을 보면 2100 근처 그리고 지금.

2015년 8월 월의 경우, S & P는., 2113의 1867의 낮은 1972의 가까이 높은 보았다 이 달의 범위가

11.64 %로, 의미 최종 손실은. 6.67 %였다 그냥 12 월에로 2000 년과 2008 년 1 월, 우리는

거의 확실하게 돌이켜 보면 다시보고 및 2015 년 8 월이 가장 최근의 상승 시세의 끝을 표시 것을

볼 수있을 것이다. 그것은 2135의 가장 최근의 피크가 올해 월에의에서, S & P는 현재 약 50 %

하락할 것입니다 ... 역사의 반복을해야 우리가 왜 그것을하지 말아야 이유 ... 다음 12~18개월

이상을 볼 수 없습니다. 이 것 늦은 2016 년 다시 아래 1,000-1,100 범위에 언젠가으로

인덱스를 가져온다.

따라서 행동 할 시간은 지금이다. 당신은 블룸버그와 CNBC의 hopium를 마시 계속 할 수

있습니다 또는 당신은 "죽음 촛불"존중과 2000 년과 2008 년에 유사한 손실을 방지하기

위해 조치를 취할 수 있습니다.

A Death Candle for the S&P 500

Past performance is not always a reliable indicator of future results. In this case, however, it very well may be. Therefore if you have stock market exposure, either through mutual funds or your 401(k), you definitely want to make note of this long-term chart.

Click to enlarge to chart below and take a good look. When you're finished, keep reading and we'll explain what you see:

Above is a 25-year, monthly chart of the S&P 500. Note that the general trend is positive but it is marked by two, significant bear market corrections.

First, note the rally that began in 1995 near the 450 level on the S&P and extended all the way to a rounded top near 1,500 over an eight-month period in 2000 when the buying momentum was finally exhausted and the market began to roll over. Often, market tops are noted with clear 20/20 hindsight and this was soon to be the case here. Note the big, nasty "Death Candle" on the chart for December of 2000. To make it easier to find, we've marked the chart with a blue arrow.

In December of 2000, the S&P saw a high of 1,389, a low of 1,254 and a final close of 1,320. This meant that, for the month, the range was 9.72% and the final loss was 4.97%. This painted a nasty, red candle on the chart that again, with the benefit of hindsight, clearly marked the trend change and the end of the bull market. By the time the S&P bottomed in October of 2002, the index had fallen to a low of 769. The total drop from the peak of 1,553 in March of 2000 to the low of just 769 in October 2002 was just over 50%.

From those 2002 lows, however, a new bull market rally began. It lasted just over five years and it peaked in November of 2007 at S&P 1,546. Once again, the stock market was forming a 6-8 month rounded top and it began to roll over in early 2008. Now please locate the middle blue arrow on the chart above. Note that it is pointing at the month of January 2008 and the big, nasty "Death Candle" found there.

In January of 2008, the S&P saw a high of 1,472, a low of 1,270 and a final close of 1,378. This meant that, for the month, the range was 13.72% and the final loss was 6.38%. Just as in December of 2000, this "Death Candle" marked the end of the bull market and beginning of a steep, painful correction. From a high of 1,546 in November of 2007, the S&P fell to a low of 667 in March of 2009. That's a total drop of 56.86%. Yikes!

Which brings us to present day and the third blue arrow on the chart that is pointing to the just-completed month of August 2015. Once again, the S&P appears to have completed a 6-8 month rounded top, failing on multiple occasions to breach stout resistance near 2100. And now look at what has been painted onto the chart...another Death Candle.

For the month of August 2015, the S&P saw a high of 2,113, a low of 1,867 and a close of 1,972. This meant that, for the month, the range was 11.64% and the final loss was 6.67%. Just as in December of 2000 and January of 2008, we will almost certainly be able to look back in hindsight and see that August of 2015 marked the end of the most recent bull market. Should history repeat...and we see no reason why it shouldn't...over the next 12-18 months, the S&P will now fall about 50% from it's most recent peak of 2,135 in May of this year.This would bring the index back down to 1,000-1,100 range by sometime in late 2016.

Therefore, the time to act is now. You can either continue to drink the hopium of Bloomberg and CNBC or you can respect "The Death Candle" and take action to avoid losses similar to 2000 and 2008.

@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

당신은 주식 시장 만이 "죽음의 십자가"를 결성 걱정해야 하는가?

세계 경제는 실속 것으로 보인다 ...

어제, 우리는 한국의 수출은 금융 위기 이후 ... 지난 8 월 이래 가장 큰 감소를

14.7 % 감소 소식이있어.이는 경제학자들이 예상 한 5.9 % 하락보다 훨씬 더 나쁘다.

그들은 세계 경제에 대해 "탄광의 카나리아"로 간주하고 있기 때문에 한국의 수출은

중요하다. 한국은 중국, 미국, 일본 등 세계에서 가장 큰 경제의 주요 수출국이다.

한국은 또한 훨씬 이전에 다른 주요 국가보다 수출 번호를 해제합니다. 한국의

수출에 대한 나쁜 독서는 세계 경제가 문제가 있다는 첫 번째 징후는 종종 이유입니다.

못생긴 소식은 전 세계의 주식을 비난했다. 중국어 주식 일본 주식은 3.8 % 하락 ...

1.3 % 하락 ... 독일, 영국, 프랑스, 스페인의 주요 지수는 모두 2 % 이상을 잃었다.

• 이 큰 방울은 일일 3 년의 글로벌 주식에 대한 최악의 달 후 온 ...

일반 케이시 독자는 지난 달의 투매가 지구상의 모든 주요 주식 시장에 충돌 알고있다.

중국 상하이 지수는 일본의 니케이 지수는 7.4 %를 잃었다 ... 12 % 손실 ...

유럽의 STOXX 600은 8.5 %를 잃었다.

MSCI 모든 컨트리 지수, 글로벌 주식 시장의 광범위한 측정, 6.8 % 하락 ...

최악의 달 2012 년부터.

미국 주식은 하드 떨어졌다. S & P 500은 8 월에 6.3 %를 잃었다. 그리고 다우 존스

산업 평균 지수는 6.6 % 하락했다. 그것은 2010 년 5 월부터 다우 최악의 달이었다,

17 년 만에 최악의 8월.

• 곰 징후가 사방에 진열되어 ...

지난 달의 충돌은 중요한 장기 추세선 아래에있는 S & P 500 떨어졌다.

장기 추세선 시장 향하고 일반 방향을 나타낸다. 많은 전문 상인은 더 큰 무언가에서

정상 시장 선회를 분리하는 데 사용합니다. 이라고 생각 "모래에 선."

투매가 장기 추세선 아래의 주식 시장을 노크 할 때 시장은 지속적으로 위아래

것입니다 ...하지만 한 우리가 장기 추세선 위에있는 한, 지배적 인 추세는 여전히

"최대."하지만, 그건 추세가 아래로까지에서 변경 될 수 있습니다 로그인합니다.

당신이 아래의 표에서 볼 수 있듯이, 금요일에 2011 년 이후 몇 "정상"selloffs가

있었다, 그러나, S & P는 약 4 년 만에 처음으로 장기 추세선 아래로 떨어졌다.

• 깨진 추세선이 지금 우리가 볼 수있는 유일한 약세 기호 아니지만 ...

미국 주식도 매우 비싸다.

로버트 쉴러는 예일 대학에서 경제학 교수 및 널리 존경받는 시장 관찰자이다. 쉴러는

가장 케이프 (을 주기적으로 조정 된 가격 실적) 비율을 만들기위한 알려져있다.

그것은 인기있는 가격 대비 수익 (P / E) 비율의 사촌이다.

P / E 비율은 실적 - 주당 (EPS)는 지난 해에 의해 인덱스 또는 주식의 가격을

나눕니다. 높은 비율은 주식이 비싼 의미합니다. 낮은 비율은 주식이 싼 것을 의미한다.

케이프 비율은 하나의 조정과 가격 / 수익 비율입니다. 대신 소득의 1 년을 사용하여

, 그것은 지난 10 년 실적을 통합합니다. 이 붐과 경기 침체의 영향을 원활하게하고

우리에게 주식이나 시장의 유용한 장기 전망을 제공합니다.

지금, S & P의 케이프 비율은 ... 약 48 % 더 비싼 1881 이후의 평균보다 24.6입니다.

• 미국 주식은 시간의 소수 더 비싼되었습니다 ...

쉴러는 그가 최근에 걱정 이유를 설명 뉴욕 타임즈 특집 :

미국의 1881 년 및 2015 년 사이의 평균 케이프 비율은 17; 7 월은 그 다음의

모든 인스턴스 세에서 1929, 2000 년과 2007 년의 주식 시장의 피크를 둘러싼

년을 포함, 매우 몇 번 발생보다 27 레벨 이상에 도달, 주식 시장은 결국 붕괴.

S & P의 케이프 비율이 역사적 평균 감소를 들어, S & P는 약 1,300에 드롭해야합니다

즉, 현재의 가격에서 최악의 34 % 급락 할 것이다.

명확하게하기 위해,이 충돌이 임박 의미하지 않는다. 어떤 통계와 마찬가지로,

케이프 비율은 완벽하지 않습니다. 케이프 장기 추세를 파악하고 도움이됩니다,

하지만하지 "시간"시장 수 있습니다.

그러나 높은 케이프 비율은 당신이 지금 미국 주식에 투자에 대한 추가주의해야합니다

하나 더 이유입니다.

• 그것은 또한 당신이 준비하는 조치를 취해야한다 의미 ...

우리는 화요일 오후에 쓰기로, 전 세계 주식 시장이 자유 낙하에 있습니다. S & P 500은

Should You Worry That the Stock Market Just Formed a “Death Cross”?

The world economy appears to be stalling…

Yesterday, we got news that South Korea’s exports dropped 14.7% since last August...their largest decline since the financial crisis. It’s far worse than the 5.9% drop economists were expecting.

South Korea’s exports are important because they’re considered a “canary in the coalmine” for the global economy. South Korea is a major exporter to the largest economies in the world including China, the US, and Japan. South Korea also releases its export numbers much earlier than other major countries. That’s why a bad reading for South Korean exports is often the first sign that the global economy is in trouble.

The ugly news slammed stocks around the world. Chinese stocks dropped 1.3%…Japanese stocks dropped 3.8%…and the major indexes in Germany, the United Kingdom, France, and Spain all lost at least 2%.

• These big drops came one day after the worst month for global stocks in over three years…

Regular Casey readers know last month’s selloff hit every major stock market on the planet. China’s Shanghai index lost 12%...Japan’s Nikkei lost 7.4%…and Europe’s STOXX 600 lost 8.5%.

The MSCI All-Country Index, a broad measure of the global stock market, fell 6.8%...its worst month since 2012.

US stocks also fell hard. The S&P 500 lost 6.3% in August. And the Dow Jones Industrial Average fell 6.6%. It was the Dow’s worst month since May 2010, and its worst August in 17 years.

• Bearish signs are popping up everywhere…

Last month’s crash dropped the S&P 500 below an important long-term trend line.

A long-term trend line shows the general direction the market is heading. Many professional traders use it to separate normal market gyrations from something bigger. Think of it as a “line in the sand.”

The market is constantly going up and down…but as long as we’re above the long-term trend line, the dominant trend is still “up.” But when a selloff knocks the stock market below its long-term trend line, it’s a sign the trend might be changing from up to down.

As you can see from the chart below, there have been a few “normal” selloffs since 2011. On Friday, however, the S&P dropped below its long-term trend line for the first time in about 4 years.

• The broken trend line isn’t the only bearish sign we see right now...

US stocks are also very expensive.

Robert Shiller is an economics professor at Yale University and a widely respected market observer. Shiller is best known for creating the CAPE (Cyclically Adjusted Price Earnings) ratio. It’s a cousin of the popular price-to-earnings (P/E) ratio.

The P/E ratio divides the price of an index or stock by its earnings-per-share (EPS) for the past year. A high ratio means stocks are expensive. A low ratio means stocks are cheap.

The CAPE ratio is the price/earnings ratio with one adjustment. Instead of using just one year of earnings, it incorporates earnings from the past 10 years. This smooths out the effects of booms and recessions and gives us a useful long-term view of a stock or market.

Right now, the S&P’s CAPE ratio is 24.6…about 48% more expensive than its average since 1881.

• US stocks have only been more expensive a handful of times…

Shiller explained why he’s worried in a recent New York Times op-ed:

The average CAPE ratio between 1881 and 2015 in the United States is 17; in July, it reached 27. Levels higher than that have occurred very few times, including the years surrounding the stock market peaks of 1929, 2000 and 2007. In all three of these instances, the stock market eventually collapsed.

For the S&P’s CAPE ratio to decline to its historical average, the S&P would have to drop to around 1,300. That would be a disastrous 34% plunge from today’s prices.

To be clear, this doesn’t mean a crash is imminent. Like any metric, the CAPE ratio isn’t perfect. CAPE is helpful for spotting long-term trends, but it can’t “time” the market.

But the high CAPE ratio is one more reason you should be extra cautious about investing in US stocks right now.

• It also means you should take steps to prepare…

As we write on Tuesday afternoon, stock markets around the world are in a free fall. The S&P 500 dropped another 3% today.

On top of that, the current bull market in US stocks is now one of the longest in history. It’s already two years longer than the average bull market since World War II.

And as we’ve explained, according to the CAPE ratio, US stocks are overpriced.

We can’t tell you for sure when the next financial crisis will hit. No one can.

But we do urge you to prepare. What’s happening right now shows how fragile the markets are. You shouldn’t ignore the mounting evidence that our financial markets just aren’t healthy.

We lay out every step you should take to prepare for the next financial crisis in our book, Going Global 2015.

This important book shows you how to get your wealth out of harm’s way and profit from the next financial disaster. It’s must-read material for anyone who’s serious about “crisis-proofing” their wealth. Right now, we’ll send it to you for practically nothing…we just ask that you pay $4.95 to cover processing costs. Click here to claim your copy.

Chart of the Day

The S&P 500 just made a “death cross.”

The death cross is a bearish chart pattern that’s supposed to predict stock market crashes. It happens when the 50-day moving average of the S&P 500 crosses under the 200-day moving average.

Investing website TheIrrelevant Investor recently looked into the history of the death cross to see if it’s really a useful indicator…

Over the last 50 years, a death cross has formed before each of the S&P 500’s ten worst years, according to The Irrelevant Investor. So the death cross is a useful indicator that something badmight happen.

However, of the 26 death crosses in the past fifty years, 73% were false positives where the stock market didn’t go on to lose even 10%.

The verdict: don’t completely ignore the death cross. It’s definitely a bad sign…especially sincethere's so much other evidence mounting that the stock market is extremely fragile right now.

However, we would pump the brakes on declaring that a death cross means a crash is imminent.

작은 캡 주식의 죽음 크로스 '바이러스 숨길 수 없습니다

작은 캡 주식의 죽음 크로스 '바이러스 숨길 수 없습니다

나스닥 종합 2-3주에 대한, 여전히 안전

나스닥 종합 2-3주에 대한, 여전히 안전