우리가 지난 가을부터 추적 한 글로벌 디플레이션 파도가 증기를 따기입니다. 이는 글로벌 유동성 거품의 자연과 피할 수없는 후유증이 당신에게 세계의 주요 중앙 은행의 호의를 가져이다. 무엇 상승하는 것은 아래로 와야합니다 - 그것은 엷은 이야기에 지나지의 내장과 hopium과 팽창 세계의 많은 저조한 건설 금융 거품, 특히 사실입니다. 이것이 의미하는 것은 금융 시장의 전통적인 여름 소강 상태가 비정상적으로 활성화하고 흥미로운 달에 8 월 설정 한 것입니다. 8 월, 그것은 나타납니다, 새로운 10월입니다. 이벤트가 너무 빨리 전개하고 있지만 시장은 지금 충돌 모드에서 확실히 가능하다 - 통화 스파이크, 주식 판매 오프, 신흥 시장 완패과 전위, 그리고 상품의 감소 - 그것은 확실히 말할 어렵다있다. 그러나,이 경우 바로 이전과 큰 시장 하락시 보통이다. 당신이 더 읽기 전에, 당신은 아마 피크 번영에, 우리의 시장 전망은 몇 년 동안 매우주의 중 하나를하고있다, 알고해야한다. 우리는 그것의 대부분은 자연의 순수 통계 때문에 소위 "복구"로 구입하지 않고, 심하게 왜곡 고문 '통계'가 믿을 수에 의존해야했다 않았다. 그래, 거짓말 아마 대부분의 경우보다 정확한 용어입니다. 또한, 중앙 은행에 의해 조작 된 금융 자산에서 이익의 대부분은 허위 및 버스트 운명 그들이 거품 심리학, 실제 돌려줍니다 기반으로했다 때문이다. 당신은 어떤을 물어 거품? 거의 너무 많은 추적 할 수 있습니다. 그러나 여기에 주요 것들이다 :

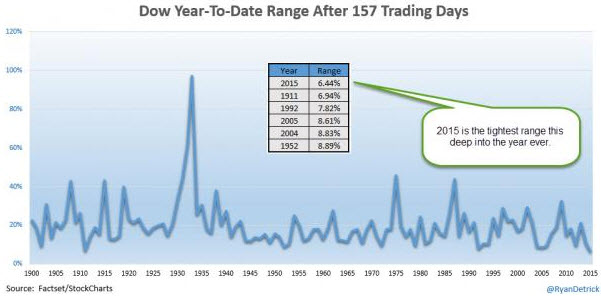

이러한 거품을 모두 함께 결합하는 것은 무엇입니까? 중앙 은행이 돈을 인쇄. 배턴을 전달지금 상주 공모에서 작동, 세계 주요 중앙 은행이 다시 후 유럽을 통해, 다시 미국에 후, 유럽, 일본에서 후, 처음으로 미국에서 일본으로, 앞뒤로 그들 사이의 유동성 지휘봉을 통과시켰다. 끝없이 항상 그들이 어떻게해야하고 무엇을하지 않았다 양적 완화의 라운드, 그들이 할 의도되지 않은 일을 많이합니다. 수조와 수조 달러를 인쇄하는 목적은 (아마도), 경제 성장을 만들 실업을 절감하고, 적당한 인플레이션 토크 것이 었습니다. 그 전선에서, 결과는 각각, 제 실력 끔찍한, 비효율적이었다. 그러나, 그 결과는 모든 실력 없었다. 연준의 먹이 통의 전면에있는 스스로에 기록 보너스를 더버기 동안 큰 은행은 횡재 수익을 거두었. 동네 짱 부자는 기록 된 역사에서 자산 이익에서 가장 큰 증가를 즐겁게하고, 정부는 극단적 인 수준의 적자 지출에 허용 저렴하고 싼 가격에 더 많은 돈을 빌릴 수 있었다. 그러나 상단에 그 파티의 모든 법안으로 인해 올 때 '작은 사람'에 대한 엄청난 비용을해야 할 것입니다. 그리고 그것은 항상 인해 온다. 돈 인쇄 가짜 재산입니다; 이 거품을 일으키고, 거품 대답해야 하나 질문이있다 버스트 때손실을 먹을거야 누가? 그리스의 가난한 서민은 지금 사용하는 그리스어 부채 GDP의 실제 상태를 숨기고에서 일괄 골드만 삭스의 공모에 의해 도움을 프랑스와 독일 은행의 소수의 실수에 대한 지불 책임이 있음을 발견한다 정교한 오프 대차 대조표 파생 헛소리. 직접적인 결과로, 그리스의 사람들이 자신의 공항, 포트, 전기 배선 및 전화 네트워크를 잃는 과정에서 '개인 투자자'- 그리스인들이 자신의 이름에 남아있는 마지막 현금 창출 자산을 수확 주로 외국인. 깨진 시장우리가 한 것처럼 반복 상세한 , 우리의 "시장은"더 이상 시장과 유사합니다. 그들은 그래서 그들은 더 이상 정말 합법적 인 시장을 자격이 없다는 것을, 중앙 은행의 정책과 과학 기술 중심의 부정 행위에 의해 모두, 왜곡됩니다.따라서 우리는 우리가 그것을 사용할 때 종종 ""시장 ""단어 주위에 이중 인용 부호를 넣어으로 촬영했습니다. 즉 그들이 해지고 얼마나 나쁜입니다. 정상적인 시장, 오늘 ""시장은 "정당한 가격 발견을위한 장소 어디"컴퓨터가 눈 깜짝 할 사이에 스크랩을 통해 서로 전투 장소, '투자자'힌지 그들의 결정은 연준이 또는하지 않을 수 있습니다 무엇을 기반으로 다음과 합리화는 설명 할 수없는 시장 가격의 움직임을 이해하는 이유에 대해 언론에 의해 종종 걸음된다. 대신, 우리가 누구의 기술 및 시장 정보를 우리의 일생에서 가장 치우치는 연주 필드 중 하나 만든 거대한 시장 지배 기업은 ""시장 ""의 점점 놀이터를 볼 수 있습니다. 이러한 왜곡의 징후가 풍부하다. 하나 완전히 이상한 차트 (YTD) 다우 지수의 평균 거래 범위는 (금주의 시장 혼란 히트 전) 지난 주에의 역사에서 가장 낮은 것을 보여주는,이 중 하나입니다. 그리고 그리스, 중국, 양적 완화, 일본, 기름의 침체, 우크라이나, 시리아,이란과 다른 넓은 시장을 교란 뉴스의 모든에도 불구하고 있었다 :

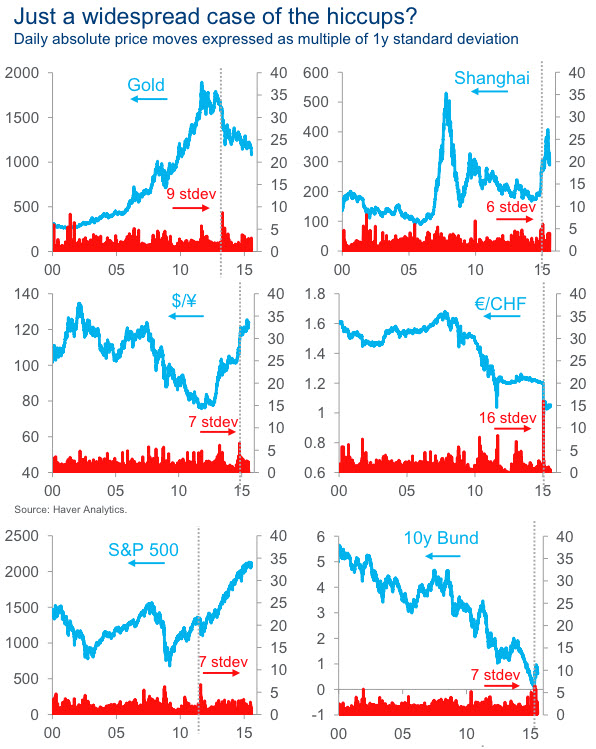

( 소스 ) 위의 차트를 기반으로, 당신은 최대 월 중순 2015 마지막 1백20년의 가장 고요한 년이라고 생각할 것이다. 물론, 고요한 아무것도하지만이었다. 이 잠긴 무역 범위에 대한 설명은 초저 거래량 및 기계의 상승의 조합이다. 시장 규모의 거의 100 %가 서로에 대한 재생 단지 기계 때 최근에 시간이되었습니다 ... 실제 투자자 (즉, 인간은 ) 포함되지 않았다. 만큼 충분한 유동성이 있다는 사실, 그 기계는 단지 ""시장 ""와 함께 탁구를 재생 만족했다. 이들이 최근 매각 보류했다 전에 2,100 선 위로 13 번 S & P 500을 건너했다. 하지만 깨진 시장을 가지고에 대한 가장 관련된 부분이 아니다. 이제까지 사실 시장에서 발생해서는 안 일이 ""시장 ""오늘날의 모든 시간이 일어나고 있다는 사실에 가장 관련된 것은 센터. 이것의 한 측정은 이벤트가 떨어져 평균으로부터 얼마나 표준 편차 (STD의 DEV) 많은 것이다. 금융 자산 가격이 0.25 %의 성병 DEV와 연간 1 %의 평균, 이동된다면,이를 2 %, 또는 3 %에 대한 약간 특이한 것이다. 이 많은 6 % 또는 7 %로 이동 한 경우 그러나 그것은 매우 이례적인 것이다. 통계는 3 표준 dev에 움직임이 매우 어렵다 일이 일어나고의 0.1 %의 확률을 갖는 우리에게 알려줍니다. 우리는 6 표준 개발자들에 도착할 때까지는, 기회는 우리가 측정하는 것은 약 한 번씩 1,300,000,000년 발생해야 너무 작습니다. 7 표준 dev에에서, 기회는 매 3까지 한 번 점프 억 년. 왜 그런 말도 안되는 수준으로 가져가? 그 이벤트의 종류가 지금 "우리" "마켓"에서 항상 발생하고 있기 때문에.이 제이미 다이 먼, JP 모건의 CEO이었다으로 그리고 깊이, 모든 사람에게 직결되어야한다 :

씨 다이 먼 은행 규제가 비난 어떻게 든 있다고 제안하는 이벤트를 사용하는 동안, 그 설명은 자체 봉사하고 솔직하다. 그는 시도하고 은행 규제를 비난하는 어떤 변명을 사용하십시오; 그 그의 일이다, 나는 생각한다. 대신 무슨 일이 우리의 ""시장 ""구조가 그렇게 그 중 하나가 '한 번에 3 억에서 몇 년 이벤트'결과 것을, 너무 심하게 그들의 조명 빠른 반사 신경에 의해 왜곡 볼륨, 컴퓨터 거래 알고리즘에 의해 왜곡되는 것이 었습니다. 인간은 여전히 거래를하고있는 사람이라면 이것은 단순히 일어나지 않았을 것입니다,하지만 그들은하지 않습니다. 모든 색깔의 재킷은 CME에서 끊었되었고, 알고리즘 이제 쇼를 실행으로 뉴욕 증권 거래소의 바닥에 인간의 마켓 메이커는 급속하게 떨어져 석양에 미끄러 있습니다. 컴퓨터에 대한 좋은 소식은 우리의 거래는 아마도 더 나은 가격 발견과 함께, 빠르고 저렴 할 수 있다는 것입니다.나쁜 소식은 아무도 정말 그들의 전체 연결 우주가 상호 작용하고는, 때때로, 그들은 견과류를 이동하는 방법을 이해하지 않는다는 것이다. 씨 디몬은 암시 된 바와 같이, 그들 인증 금융 붕괴로 다음 회계 침체를 측정하고 그 변환의 기회를 가질 얼마나 흔한이 '억 년 이벤트'인가? 그들은 지금 모든 시간을 일. 여기에 짧은 목록입니다 :

( 소스 ) 이 모든 것은 매우 심각한, 시장 파열 사고의 기회뿐만 아니라 가능하다는 결론을 우리를 인도하지만, 확률은 비교적 짧은 시간 지평을 통해 100 %에 접근하는 것이. 우리가 경고했습니다 디플레이션 문에 지금이다. 그리고 우리의 큰 관심사 중 하나는 우리가 대신 ""시장 ""가지고 있다는 것입니다 시장에 우리가 알고 그것을 사랑하는 일이 우리의 금융 시스템을 깰 수 있다는 것을 의미한다. 외부에서부터피크 번영에서 우리의 주요 운영 모델 중 하나에 문제가 시작될 때 항상 에지에서 시작하고, 외부로부터의 이동한다는 것이다. 이것은, (푸드 뱅크 비싼 주택 가격 하락도 전에 수요 스파이크 참조) 부문의 주식 (가장 약한 회사가 먼저 감소), 채권 (정크 채권 수익률 처음 스파이크) 당신이 사회에서 사람들을 찾고 있습니다 여부를 사실이다 또는 약한 국가가 먼저 문제가 얻을 전 세계에 걸쳐. 우리가 지금보고있는 것은 특히 빠른 너무 빨리 그들 모두를 추적하기는 어렵습니다 자르기되는 지표 '외부에'의 설정 움직이고있다. 여기에 가장 큰 것입니다. 환율 쇠퇴시장 (EM) 통화 신흥 최근 하락은 거대한 붉은 깃발입니다. EM 외환이 결합 된 차트는 말의 확대 하락을 보여줍니다.

( 소스 ) 지난 월요일 이후, 여기에 추악한 진실이다 :

이들 국가의 대부분은 시도하고 자국 통화의 급격한 하락을 막기 위해 귀중한 외환 보유액을 사용하고있다, 그러나 나는 대학살이 끝난 전에 모든 탄약 부족하게됩니다 우려하고있다. 여기에서 일어나고있는 것은 서쪽 중앙 은행 해방하는 유동성 홍수의 반대 부분이다. 이 사이클의 선순환 부분은 투자자들이 유럽, 미국이나 일본에서 싸게 돈을 빌릴하고 일반적으로 국채를 구입, 또는 현지 기업에 투자 (특히 원자재 붐의 오프 번들을함으로써, EM 국가의 공원보고 그 ) 발생했다. 그래서 도덕적 인 측면에서 주요 통화 빌린 후 참여했다 로컬 어떤 EM 통화 구입하는 데 사용되었다 (이 해당 통화의 가치를 운전) 한 다음 로컬 자산은 주식 시장을 운전 또는 아래로 운전 중 어느 팔렸다 (가격에 역에서로 이동) 채권 수익률. 사이클의 선순환 부분은 현지 기업과 정치인에게 사랑 받고 있습니다. 모든 것이 잘 작동합니다. 통화는 상승, 채권 금리가 떨어지고, 주식이 상승하고 안정적이며, 모든 사람이 일반적으로 행복하다. 그러나 웜은 회전 할 때, 그것은 항상,이주기, 악순환 부분의 뒷면을 수행, 정말 아파하고 우리가 지금보고있는거야. , 투자자들은 충분한 충분 결정, 그래서 그들은 지역의 채권 및 주식 그들이 구입 (그래서 주식 시장 하락과 금리 상승) 가격 아래로 모두 운전을 판매하고 달러 또는 엔이나 유로에 대한 대가로 현지 통화를 판매 중은 처음에 빌린했다. 그리고 이렇게 우리는 떨어지는 EM 통화를 참조하십시오. 위에 나열된 통화의 대부분은 지금 수준에서 거래되고, 상황이 말하면 하나없는 1997 년 아시아 외환 위기 이후 볼, 또는 수준에서 이전에 전혀 본 적이 없다. 가난한 멕시코 페소 일찍 달러 오늘 아침 (16.9950)에 바로 올해 12 % 하락, 거의 17로했다 참여 통화 중 하나입니다. 페소를 연타하면 내년 멕시코 연방 정부의 예산을 파괴하는 궤도에 절대적으로 석유의 낮은 가격입니다. 주식 시장의 쇠퇴통화와 콘서트에서 우리는 주변 주식 시장에 깊은 고통을보고있다 풀릴. 지금이 있습니다 20 개 이상의 그들의 피크에서 20 % 이상의 하락을 겪었다 한 의미 '곰 국가에 있는지. 여기에 브라질 최악의 형태로 존재하여, 몇 가지 선택 것들이다 :

이러한 징후의 모든 위대한 중앙 다시 유동성 쓰나미는 과정을 역으로 피해를 많이 만들고 바다에 쓰레기를 많이 흡입하는 것입니다 것을 생각을 강화한다. 상품 대승EM 국가의 많은 상품 수출하고 있습니다. 그들은 우리가 가장 먼저 중국에 의미있는 세계의 나머지, 자신의 미네랄 나무와 바위를 판매하고 있습니다. 상품은 바로 가격면에서 심하게 일을하지 않는, 그들은 절대적으로 분쇄되고 지금 지난 4 년 동안 일부 50 % 아래로있다.

( 소스 ) 상품은 EM 경제 행복이나 고통의 정도 외에 여러 가지를 알려줍니다 - 세계 경제가 성장 또는 축소 여부를 그들이 우리에게 알려줍니다. 지금 그들이 말하는 실력을 결과 (경기 침체)에 일본, 유럽과 미국에서 나오는과 함께, 최근 중국어 수입, 수출 및 제조의 모든 데이터에 의해 확인되는 "축소"입니다. 결론 부우리는 오랜 시간 동안 경고했습니다, 당신은 번영에 당신의 방법을 인쇄 할 수 없습니다, 당신은 단지 상승 시간을 거래하여 불가피을 지연시킬 수 있습니다. 우리는 2008 년에, 우리는 이미 제로에 붙어 책과 금리에 $ 200 조원이 다음 위기를 입력하고 그랬던 것처럼 지금, 대신 찾는 자신 글로벌 부채 $ 155 조원에 안장. 우리는 30피트 대신 10의 사다리까지이며, 그것은 아래로 긴 방법입니다. 어떤 도구는 중앙 은행이 정말 지금에 외부에서 금융 풍경을 가로 질러 뛰어 놀고있다 디플레이션의 힘 싸움을 떠난합니까? 컴퓨터는 딸꾹질 우리에게 스매싱 또는 시장이 8 시그마는 정부가 무엇을 할 것인가 이동 파열 일부 기관을주는 경우에? 시장을 종료? 그것은 가능성, 그리고 당신이 준비해야하는 하나. 어디 우리가이 향하고 있는가? 지금 매장은 기본 공급의 깨끗한 제거됩니다 인플레이션 재해에 연루되어 베네수엘라의 희망이 아닌 방법은, 사회 불안은 때문에 창조적 인 노점상 지금, 말 그대로,보다 훨씬 저렴 2 볼리바르 노트에 싸여 empanadas입니다을 판매 성장 및 냅킨. 클리너? 어쩌면 순전히. 나는 통화 떨어져 먹고 싶지 않을 것이다.

( 소스 ) 그러나 실수하지, 모든이에 대한 최종 결과는 루드비히 폰 미제스, 오스트리아 경제학자에 의해이 인용에서 훌륭하게 캡처 :

신용 확장 1980 년과 2008 년 사이에 일어난이 온전 무지 중앙 은행에 의해 무시 된 경고 사격이었고, 지금 우리가 가진 부채는 주장이 더하지 덜 수 있습니다. 베네수엘라는 이미 통화에 대한 '총 재앙'단계에 진입하고 있지만 것 모두가 결국 자발적으로 신용 창조에 의해 활성화 붐의 달콤한 구제를 포기하는 자체가없는 발견 국가에 살고있는 사람으로 일본을 따라 따릅니다. Making Sense Of The Sudden Market PlungeThe global deflationary wave we have been tracking since last fall is picking up steam. This is the natural and unavoidable aftereffect of a global liquidity bubble brought to you courtesy of the world’s main central banks. What goes up must come down -- and that's especially true for the world's many poorly-constructed financial bubbles, built out of nothing more than gauzy narratives and inflated with hopium. What this means is that the traditional summer lull in financial markets has turned August into an unusually active and interesting month. August, it appears, is the new October. Markets are quite possibly in crash mode right now, although events are unfolding so quickly – currency spikes, equity sell offs, emerging market routs and dislocations, and commodity declines - that it’s hard to tell for sure. However, that’s usually the case right before and during big market declines. Before you read any further, you probably should be made aware that, at Peak Prosperity, our market outlook has been one of extreme caution for several years. We never bought into so-called "recovery" because much of it was purely statistical in nature, and had to rely on heavily distorted and tortured 'statistics' to be believed. Okay, lies is probably a more accurate term in many cases. Further, most of the gains in financial assets engineered by the central banks were false and destined to burstbecause they were based on bubble psychology, not actual returns. Which bubbles you ask? There are almost too many to track. But here are the main ones:

What’s the one thing that binds all of these bubbles together? Central bank money printing. Passing The BatonOperating in collusion, the world's major central banks passed the liquidity baton back and forth between them, first from the US to Japan, then from Japan to Europe, then back to the US, then over to Europe again where it now resides. Seemingly endless rounds of QE that didn’t always do what they were supposed to do, and plenty of things they were not intended to do. The purpose of printing up trillions and trillions of dollars (supposedly) was to create economic growth, drive down unemployment, and stoke moderate inflation. On those fronts, the results have been dismal, horrible, and ineffective, respectively. However, the results weren’t all dismal. Big banks reaped windfall profits while heaping record bonuses on themselves for being at the front of the Fed’s feeding trough. The über-wealthy enjoyed the largest increase in wealth gains in recorded history, and governments were able to borrow more and more money at cheaper and cheaper rates allowing them to deficit spend at extreme levels. But all of that partying at the top is going to have huge costs for ‘the little people’ when the bill comes due. And it always comes due. Money printing is fake wealth; it causes bubbles, and when bubbles burst there’s only one question that has to be answered: Who’s going to eat the losses? The poor populace of Greece is just now discovering that it collectively is responsible for paying for the mistakes of a small number of French and German banks, aided by the collusion of Goldman Sachs, in hiding the true state of Greek debt-to-GDP using sophisticated off-balance sheet derivative shenanigans. As a direct result, the people of Greece are in the process of losing their airports, ports, and electrical distribution and phone networks to ‘private investors’ -- mainly foreigners harvesting the last cash-generating assets the Greeks have left to their names. Broken MarketsAs we’ve detailed repeatedly, our “markets” no longer resemble markets. They are so distorted, both by central bank policy and technologically-driven cheating, that they no longer really qualify as legitimate markets. Therefore we’ve taken to putting double quote marks around the word “”market”” often when we use it. That’s how bad they’ve become. Where normal markets are a place for legitimate price discovery, todays “”markets”” are a place where computers battle each other over scraps in the blink of an eye, ‘investors’ hinge their decisions based on what the Fed might or might not do next, and rationalizations are trotted out by the media for why inexplicable market price movements make sense. Instead, we view the “”markets”” as increasingly the playgrounds of, by and for the gigantic market-controlling firms whose technology and market information have created one of the most lopsided playing fields in our lifetimes. Signs of these distortions abound. One completely odd chart is this one, showing that the average trading range of the Dow (ytd) was the lowest in history as of last week (before this week’s market turmoil hit). And that was despite Greece, China, QE, Japan, oil’s slump, Ukraine, Syria, Iran and all of the other ample market-disturbing news:

(Source) Based on the above chart, you’d think that 2015 up through mid-August was the most serene year of the last 120 years. Of course, it's been anything but serene. The explanation for this locked-in trading range is a combination of ultra-low trading volume and the rise of the machines. There have been times recently when practically 100% of market volume was just machines playing against each other…no actual investors (i.e, humans) were involved. As long as there was ample liquidity, then the machines were content to just play ping pong with the “”market””. Which they did, crossing the S&P 500 over the 2,100 line 13 times before the recent sell-off took hold. But that’s not the most concerning part about having broken markets. The most concerning thing centers on the fact that things that should never, ever happen in true markets are happening in todays “”markets”” all the time. One measure of this is how many standard deviations (std dev) an event is away from the mean. For example, if the price of a financial asset moves an average of 1% per year, with a std dev of 0.25 %, then it would be slightly unusual for it to 2%, or 3%. However it would be highly unusual if it moved as much as 6% or 7%. Statistics tells us that something that 3 std dev movements are very unlikely, having only a 0.1% chance of happening. By the time we get to 6 std devs, the chance is so small that what we’re measuring should only happen about once every 1.3 billion years. At 7 std dev, the chance jumps up to once every 3 billion years. Why take it to such a ridiculous level? Because those sorts of events are happening all the time in our “”markets”” now. And that should be deeply concerning to everyone, as it was to Jamie Dimon, CEO of JP Morgan:

While Mr. Dimon used the event to suggest that bank regulations were somehow to blame, that explanation is self-serving and disingenuous. He'd use any excuse to try and blame bank regulations; that’s his job, I guess. Instead what happened was that our “”market”” structure is so distorted by computer trading algorithms, with volume so heavily distorted by their lighting-fast reflexes, that one of those ‘once in 3-billion years events’ resulted. This simply wouldn't have happened if humans were still the ones doing the trading, but they aren't. All the colored jackets have been hung up at the CME, and human market makers on the floor of the NYSE are rapidly slipping away into the sunset as algorithms now run the show. The good news about computers is that they allow our trading to be faster and cheaper, presumably with better price discovery. The bad news is that nobody really understands how the whole connected universe of them interact and that, from time to time, they go nuts. As Mr. Dimon hinted, they have the chance of taking the next financial downturn and converting it into a certified financial meltdown How common are these ‘billion year events’? They happen all the time now. Here’s a short list:

(Source) All of this leads us to conclude that the chance of a very serious, market-busting accident is not only possible, but that the probability approaches 100% over even relatively short time horizons. The deflation we’ve been warning about is now at the door. And one of our big concerns is that we’ve got “”markets”” instead of markets, which means that something could break our financial system as we know and love it. From The Outside InOne of our main operating models at Peak Prosperity is that when trouble starts it always begins at the edges and moves from the outside in. This is true whether you are looking at people in a society (food banks see a spike in demand well before expensive houses decline in price), stocks in a sector (the weakest companies decline first), bonds (junk debt yields spike first), or across the globe where weaker countries get in trouble first. What we’re seeing today is an especially fast moving set of ‘outside in’ indicators that are cropping up so fast it’s difficult to keep track of them all. Here are the biggest ones. Currency DeclinesThe recent declines in emerging market (EM) currencies is a huge red flag. This combined chart of EM foreign exchange shows the escalating declines of late.

(Source) Since last Monday, here’s the ugly truth:

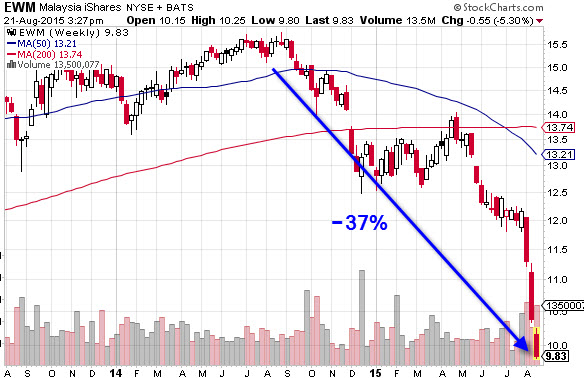

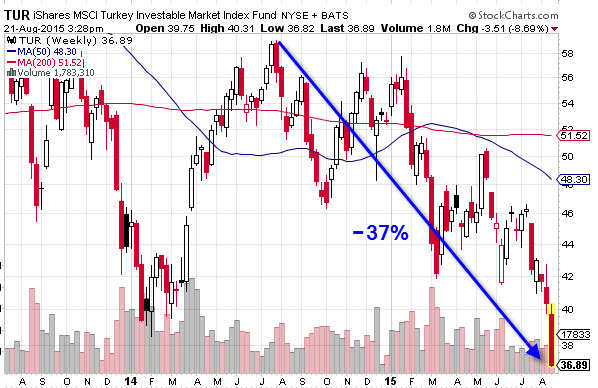

Many of these countries have been using precious foreign reserves to try and stem the rapid declines of their currencies, but I fear they will all run out of ammo before the carnage is over. What’s happening here is the reverse part of the liquidity flood that the western central banks unleashed. The virtuous part of this cycle sees investors borrow money cheaply in Europe, the US or Japan, and then park in in EM countries, usually by buying sovereign bonds, or investing in local companies (especially those making a bundle off of the commodity boom that was happening). So on the virtuous side, a major currency was borrowed, and then used to buy whatever local EM currency was involved (which drove up the value of that currency), and then local assets were bought which either drove up the stock market or drove down bond yields (which move as in inverse to price). The virtuous part of the cycle is loved by local businesses and politicians. Everything works great. The currency is stable to rising, bond yields are falling, stocks are rising, and everyone is generally happy. However when the worm turns, and it always does, the back side of this cycle, the vicious part, really hurts and that’s what we’re now seeing. The investors decide that enough is enough, and so they sell the local bonds and equities they bought, driving both down in price (so falling stock markets and rising yields), and then sell the local currency in exchange for dollars or yen or euros, whichever were borrowed in the first place. And thus we see falling EM currencies. To put this in context, many of the above listed currencies are now trading at levels either not seen since the Asian currency crisis of 1997, or at levels never before seen at all. The poor Mexican peso is one of the involved currencies, which has fallen by 12% just this year, and almost made it to 17 to the dollar early this morning (16.9950). Battering the peso is also the low price of oil which is absolutely on track to destroy the Mexican federal budget next year. Stock Market DeclinesIn concert with the currency unwinds we are seeing deep distress in the peripheral stock markets. There are now more than 20 that are in ‘bear country’ meaning they’ve suffered declines of 20% or more from their peaks. Here are a few select ones, with Brazil being in the worst shape:

All of these signs reinforce the idea that the great central back liquidity tsunami has reversed course and is about to create a lot of damage and suck a lot of debris out to sea. The Commodity RoutA lot of EM countries are commodity exporters. They sell their minerals trees and rocks to the rest of the world, by which we mean to China first and foremost. Commodities are not just doing badly in terms of price, they are absolutely being crushed, now down some 50% over the past four years.

(Source) Commodities tells a number of things besides the extent of EM economic happiness or pain – they tells us whether the world economy is growing or shrinking. Right now they are saying “shrinking” which is confirmed by all of the recent Chinese import, export and manufacturing data, along with the dismal results coming out of Japan (in recession), Europe and the US. Conclusion Part IAs we’ve been warning for a long time, you cannot print your way to prosperity, you can only delay the inevitable by trading time for elevation. Now, instead of finding ourselves saddled with $155 trillion of global debt as we did in 2008, we’re entering this next crisis with $200 trillion on the books and interest rates already stuck at zero. We are 30 feet up the ladder instead of 10 and it’s a long way down. What tools do the central banks really have left to fight the forces of deflation which are now romping across the financial landscape from the outside in? If the computers hiccup and give us some institution smashing or market busting 8 sigma move what will the authorities do? Shut down the markets? It’s a possibility, and one for which you should be prepared. Where are we headed with all this? Hopefully not the way of Venezuela which is now so embroiled in a hyperinflationary disaster that stores are stripped clean of basic supplies, social unrest grows, and creative street vendors are now selling empanadas wrapped in 2 bolivar notes because they are, literally, far cheaper than napkins. Cleaner? Maybe not so much. I wouldn’t want to eat off of currency.

(Source) But make no mistake, the eventual outcome to all this is captured brilliantly in this quote by Ludwig Von Mises, the Austrian economist:

The credit expansion happened between 1980 and 2008, there was a warning shot which was soundly ignored by ignorant central bankers, and now we have more, not less, debt with which to contend. Venezuela has already entered the ‘total catastrophe’ stage for its currency, but Japan will follow along, as will everyone eventually who lives in a country that finds itself unable to voluntarily abandon the sweet relief of booms enabled by credit creation. @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@ 왜 주식은 떨어지고있다? 이 차트는 하드 중국이 세계 시장을 강타했다 방법을 보여줍니다 이미지 : 블룸버그 왜 주식 시장은 이제 거절한다? 왜 현재의 대학살? 간단한 측면에서 현재의 혼란은 소위의 고전과 거대한 예입니다 오스트리아 비즈니스 사이클 이론 . 기본적으로 malinvestment은 인위적으로 낮은 금리에 의해 유도된다. 기업은 malinvest. 사람들은 malinvest. 정부는 malinvest. 그리고 그 아래 실제 시장 기반 가격의 소리 재단이없는 조만간이 모든 malinvestment, 투자는 축소합니다. 모든 헛소리는 전면에 온다. 현실 안타. 고통은 안타. 그것은 우리가 대규모로 지금 무엇을보고있다. 무엇 특히 우려 것은 우리가 아주 최근에, 전에 본 적이 있다는 것입니다. 2008 년을 생각하고 우리는 명확하게 우리의 교훈을하지 않았다. 충돌이 명중 할 때 중앙 은행은 시스템에서 삭제되는 그린스펀의 인위적으로 낮은 가격에서 모든 이전 malinvement을 유지 (또는 적어도 많은) "자극"과 양적 완화 정책으로 아래로 두 배. 그래서 우리는 지금 2008 년 이전 시대 malinvestment의 많은뿐만 아니라 이후 2008 충돌을 생성 된 모든 malinvestment 처리해야합니다. 아무것도 무료입니다. 모든 비용이 있습니다. 중앙 은행의 홀에서 특히 가난한 결정.

Why are Stocks Falling? These Charts Show How Hard China Has Hit Global MarketsImage: Bloomberg Why is the stock market turning down now? Why the current carnage? In the simplest terms the current chaos is a classic and colossal example of what is called the Austrian Business Cycle Theory. Basically malinvestment is induced by artificially low interest rates. Businesses malinvest. People malinvest. Governments malinvest. And then sooner or later all this malinvestment, investment which doesn’t have the sound foundation of real market based prices underneath it, collapses. All the baloney comes to the fore. Reality hits. Pain hits. That’s what we are seeing now on a massive scale. What is of particular concern is that we’ve seen this before, very recently. Think 2008. And we clearly didn’t learn our lesson. When the Crash hit central banks doubled down with “stimulus” and quantitative easing which kept all the prior malinvement (or at least much of it) from Greenspan’s artificially low rates from being cleared from the system. So we now must deal with all the malinvestment created post-2008 Crash as well as much of the malinvestment from the pre-2008 era. Nothing is free. Everything has a cost. Especially poor decisions in the halls of central banks.

@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@ 경제 위기는 주류 간다 - 다음에 무슨 일이?대안 경제 분석가들은 상품이 QE3의 테이퍼 다른 모든 금융 지표에서 저단 변속을 위해 신호를 울리고 된 직후 분쇄 및 석유 충돌 것을 경고했다 때 지난해 주류의 일반적인 반응은 우리가 과민 반응과 편집증 및 것이 있다고했다 상품의 충격은 일시적이었다. 아마도 사실은 그들이 당신을 얻기 위해 정말로 경우가 편집증이 아니라고 반복해야합니다. 짧은 시간 후, 그것은 주류 경제 예 - 남자의 수사가 변경되는 방식을 정말 놀랍습니다. 존재하지 않는 세계 경제 회복을 위해 치어 리더되었다 블라인드 분석가들은 이제 조심스럽게 폴 크루그먼의 사무실이 있어야한다 뉴욕 타임즈에서 수위의 옷장을 통해 이관되고있다. 예를 들어, 미국의 금리처럼 언론은 마지 못해 글로벌 불안정성으로 인정되는 인상은 경기 침체에 반환을 선도. (주류 미디어에 특별한주의가 :. 연준의 경기 부양을 통해 지표의 열매를 맺지 조작을 데려가, 우리가 경기 침체를 떠난 적이) 그들은 또한 지금 중국의 시장 충돌과 위안을 인정하도록 강요 평가 절하가 세계에 대한 광범위한 영향이 위기를 , 년 전에 반면 주장은 중국의 문제는 중국에 머물 것이라고했다. 심지어 중국의 자체 미디어는 이제 재정적으로 상호 의존적 인 경제의 체인 어떤 국가의 경기 침체는 모든 사람을위한 수단의 경고하고있다. MSM은 마침내의 광대 한 재정 문제 있다는 분명한 개념을 즐겁게하고 있습니다 유럽 연합 (EU)은프랑스와 이탈리아 등 주요 국가에서 채무 및 고용 문제를 분쇄 함께 할 그리스의 위기를 할 조금 더 있습니다. 그리고 갑자기, 전문가는 다시 한 번 우려되는 일본의 미니 경기 침체의 전염병과 삶의 단지 방법이 아니다 회계 수축의 진리가 아니라 정적 머물보다 더 빨리지고 지수 동적. 이 문제는 물론, 항상 광 터널의 끝에서 볼 수 있고, 그 성장이 불가피 반환 제안을 따른다. 주류 언론은 현실의 포인트를 논의 할 수 있지만, 그 동화에 혼합되는 시간에 그들을 막을하지 않습니다. 주류에서 수사에이 변화는 반드시 미디어의 각성으로 인해하지 않을 수 있습니다. 새로운 이야기가 등 엘리트 교육 기관 은행 핵심 내놓은되기 때문에 오히려 그것은있을 수 있습니다 국제 통화 기금 (IMF) 그들이 알고 경제 위기의 여파로 관할 표시하는 임무를 설립하고 국제 결제 은행, 기관이 약이다 트리거합니다. IMF는 지속적으로 인해 중앙 은행에 세계 시장에서 잠재적 인 재해에 관한 진술하고있다 자극 (이 조치 원래 옹호 혼합 전송)뿐만 아니라 잠재적 인 금리 인상을 메시지를 경건한 주류 추종자. 국제 통화 기금 (IMF)의 최신 개요 글로벌 시장은 최근까지 주류 언론보다 훨씬 gloomier왔다. 갑자기,이 매체는 국제 주의적 논점을 앵무새에 방향을 부여하고있다, 보일 것입니다. BIS는 경고 세상이 다음 시장 위기에 대한 현재 무방비 상태입니다. 나는 BIS가 경제 충돌을 예측 포함의 기록이 지적 것 다시 2007 년 파생 상품과 신용 위기가 시작되기 직전입니다. 재정 재해를 예견하는이 기능으로 인해 BIS는 글로벌 중앙 은행의 지배적 인 힘이고 사실에 훨씬 더 가능성이 원인 위기보다는 단지 위기의 예측. 즉, 당신 자신을 시작하려고 재해를 예측하기 쉬운, 말을하는 것입니다. 그것은 BIS와 국제 통화 기금 (IMF)의 경고가 너무 늦게 너무 적게 오는 경향이있다, 또는 많은 다른 분석가들은 몇 년 전에 뭐라고했는지 같은 소리 오늘주의 보도 자료를 작성하기 시작하는 것이 실수 없습니다. 이 globalist의 조직의 목표는 조니 - 온 - 최근으로 예후 인자를 붕괴 후 그들은 그 때 이유에 대한 합리화로 사용할 수있는, 그들은 우리 모두에게 경고를 주장 할 수 있도록 사람들이 준비 만 자신을 설정하는 데 도움이되지 않습니다 최고의 인재는 전체 행성의 경제를 관리하다합니다. 이제 주류가 분명 경제적 위험에보고 할 용의가 있음을, 어떻게 다음됩니까? MSM 서술의 변화는 나쁜 징조입니다. 우리가 사태의 그림자에서 잘 때까지 2008 년 파생 상품 붕괴의 초기 언론 보도는 부정적인가되지 않았다. 같은 사실 오늘을 보유하고 있다면, 시장 이벤트가 임박. 다음은 년 앞으로 간다에 대한 자세한 내용을들을 수있는 문제 중 일부입니다. 중국 '전염' 그리스어 전염 잊어, 우리는 다음 몇 개월 동안 중국어 감염에 대한 훨씬 더 듣고됩니다. 카네기 국제 평화 재단 실행 globalist의는 이미 잡지의 개념 수비된다 '외교 정책을' . 위안화의 평가 절하와 함께, 주류 분석가들은 통화 전쟁, 그들은 거의 이제까지 과거에 즐겁게하지 않는 개념의 가능성을 통해 혈안이 있습니다. 위안화 평가 절하가 필요하지만, 중국 자체에 대한 부정이 아니다. 사실, IMF는 최근 문에서 중국의 경제가 느리지 만 더 "안정"성장 "새로운 정상"를 입력되어 있다고 주장한다. IMF는 일년 내내 확장이 있지만 또한 (세계 시장에 떨어지는 위안의 최근의 충격이 실제로 통화 추가 가능한 특별 인출 권 글로벌 통화 바스켓에 포함, 11 월 완료 될 예정이다 결정하게 발표했다 ) 승인하기 전에 국제 통화 기금 (IMF)에 의해 추천되었다. 경제 뉴스는 아마도 거짓 이스트 / 웨스트 패러다임의 영속과 미국인을 설계 글로벌 은행보다는 전반적인 금융 위기에 대한 중국을 비난해야한다는 생각으로 이어지는, 올해의 나머지 중국에 논스톱 집중 될 것으로 예상 엉망. 한편, 최고 globalists는 충돌을 통해 복잡성은 위험하고, 그 상호 경제가 아래로 단순화해야한다는, "아무도의 잘못"이라고 주장 화평 케와 문제 해법으로 자신을 제시, "중립"을 유지하기 위해 계속 하나의 글로벌 통화와 단일 글로벌 권한. 미국 경제 느낌의 효과 아마 2015 전에 결정된다 금리 인상에 대한 연방 준비 제도 이사회 (FRB)의 푸시는 끝났습니다. 금리 9 월 증가 토크 계략, 테이블에있을 수 지연 막판 결정을 할 수있다. 이 가장자리 - 중 - 좌석 회의의 전술과 지연을 놀라게들은 방심 애널리스트를 많이 던져 테이퍼가 발생하지 않을 것이라고 믿는 많은 원인이 된 QE 테이퍼 시나리오 동안 사용되었다. 금리 인상이 약간 이상 주류 분석가들이 예상 한 것보다, 일이 일어날 단지뿐만 아니라, 그것은 일어날 않았다. 지연이 발생하는 경우, 그것은 실력을 소매 판매는 크리스마스 시즌으로 이어지는 부정 할 수없는 해짐에 따라 요금 12 월 전에이 증가함에 따라, 주식에서 죽은 고양이 바운스를 유발, 수명이 짧은 것입니다. 이는 연준의 작업을 보호하지, 미국 경제를 탈선하는 것을 기억하는 것이 중요하다. 위안의 포함이 널리 달러의 세계 - 예약 상태에 대한 위협으로 간주하여 한편, IMF의 SDR 회의는 계속됩니다. 주류 언론은 이제 미국 국민을 준비 (또는 적어도 어떤주의를 기울이고있는 사람들)되는 세계 - 예약 상태를 오는 손실을. 선전은 나쁜 일이 같은 달러의 예비 위치를 칠하는 것을 목표로하고있다. MSM은 예약 상태의 손실이 실제로 미국 경제가 다시 궤도에 얻을 도움이 될 수 있고 국가 통화의 글로벌 조화는 우리의 재정 전망에 후원을 할 것이라고 주장한다. 이 명확의 최종 충돌을 통해 모든 문제에 대해 대중을 접종하는 시도이다 달러 값. 유가 패닉 유가는 폐 계속하고 후 효과는 측정하기 어려울 것이다. 으로 존 케리가 공개적으로 (포함된다 수익성 석유 수출 거래 포함)이란 거래의 실패는 달러의 세계 - 예약 상태의 손실을 초래할 수 있다고 경고, 내가하지 에너지 시장의 미래 전망에 대해 매우 낙관적이다. 케리 후보는 실패한이란 계약 거래를 중개 동맹국들과 확률에 미국을 넣어 것이라고 주장하지만, 이것은 전체 이야기가 아닙니다. 정말로 일어나고있는 것은 SDR의 상승과 사우디 아라비아 곧 고독한 구매 메커니즘으로 달러에서 분리 될 가능성을 포함하여 달러의 미래에 가을의 진짜 이유, 멀리 대중을 방해하는 케리의 시도이다 그들의 석유 (사우디 아라비아는 놀랍게도 중 하나입니다 주요 지지자 이란 거래). 그것은이란 계약의 붕괴 어쨌든 일어날 달러 보유 상태의 손실에 대한 변명으로 사용될 수 있다는 것을 아마 가능하다. 빠른 이동 이벤트 경제 뉴스는 올해 매우 빠른 이동, 우리는 대안 경제 연구자들 사이의 일반적인 합의가 2015 트리거 이벤트와 죽은 환상의 해가 될 것으로 보인다 2016 년에에 폐쇄로는 더 열광적 될 것입니다. 자격 내 여섯 부분 시리즈 '실물 경제에서 마지막으로 봐 그것은 내파하기 전에' 나는 본질적으로이 시간표에 동의합니다. 2014 모든 즉각적인 경고 징후와 새로운 2007의 되었다면, 2015 모든 혼란과 깨진 패러다임과 새로운 2008입니다. Economic Crisis Goes Mainstream - What Happens Next?Last year, when alternative economic analysts were warning that the commodities crush and oil crash just after the taper of QE3 were blaring signals for a downshift in all other financial indicators, the general response in the mainstream was that we were overreacting and paranoid and that the commodities jolt was temporary. Perhaps the fact needs repeating that it’s not paranoia if they are really out to get you. Only a short time later, it is truly amazing how the rhetoric from the mainstream economic yes-men is changing. The blind analysts who were cheerleading for the nonexistent global recovery are now being carefully relegated to the janitor’s closet over at The New York Times, where Paul Krugman’s office should be. Media outlets are begrudgingly admitting to global instabilities like, for instance, a U.S. interest rate hike leading to a return to recession. (Special note to the mainstream media: Take away the fruitless manipulation of indicators through Fed stimulus, and we never left the recession.) They also are now forced to acknowledge that China’s market crash and yuan devaluation have far-reaching implications for global crisis, whereas a year ago the claim was that China’s problems would stay in China. Even China’s own media are now warning of the chain of fiscally interdependent economies and what the nation’s downturn means for everyone. The MSM are finally entertaining the obvious notion that the vast financial problems of the EUhave little to do with the crisis in Greece and more to do with crushing debt obligations and employment problems in primary nations like France and Italy. And suddenly, pundits are once again concerned with Japan’s epidemic of mini-recessions and the truth of fiscal contraction that is not just a way of life, but an exponential dynamic that is getting worse fast, rather than staying static. This concern is, of course, always followed with suggestions that the light can be seen at the end of the tunnel and that growth will inevitably return. The mainstream media may be discussing points of reality, but that does not stop them at times from mixing in fairy tales. This alteration in rhetoric from the mainstream may not necessarily be due to an awakening in the media. Rather, it may be due to the new narratives being put forth by core banking elite institutions like the International Monetary Fund and the Bank of International Settlements, institutions that have established a mission to appear competent in the wake of an economic crisis they KNOW is about to be triggered. The IMF is consistently making statements regarding potential disaster in global markets due to central banking stimulus measures (which itoriginally championed), as well as potential rate hikes, sending mixed messages to devout mainstream followers. The IMF’s latest overviews of global markets have been far gloomier than mainstream media outlets until recently. Suddenly, it would seem, the media has been given direction to parrot internationalist talking points. The BIS warns that the world is currently defenseless against the next market crisis. I would point out that the BIS has a record of predicting economic crashes, including back in 2007 just before the derivatives and credit crisis began. This ability to foresee fiscal disasters is far more likely due to the fact that the BIS is the dominant force in global central banking and is the causeof crisis, rather than merely a predictor of crisis. That is to say, it is easy to predict disasters you yourself are about to initiate. It is no mistake that the warnings from the BIS and the IMF tend to come too little too late, or that they are beginning to compose cautionary press releases today that sound much like what alternative analysts were saying a few years ago. The goal of these globalist organizations is not to help people prepare, only to set themselves up as Johnny-come-lately prognosticators so that after a collapse they can claim they warned us all, which can then be used as a rationalization for why they are the best people to administrate the economies of the planet as a whole. So now that the mainstream is willing to report on clear economic dangers, what happens next? The change in the MSM narrative is a bad sign. The initial media coverage of the derivatives implosion in 2008 did not become negative until we were well within the shadow of the avalanche. If the same holds true today, then a market event is imminent. Here are some of the issues you may hear more about as the year goes forward. China ‘Contagion’ Forget about Greek contagion, we will be hearing far more about Chinese contagion over the next several months. The globalist run Carnegie Endowment for International Peace is already fielding the concept in their magazine 'Foreign Policy'. With the devaluation of the yuan, mainstream analysts are frantic over the possibility of currency wars, a concept they rarely ever entertained in the past. Yuan devaluation is not, though, necessarily a negative for China itself. In fact, the IMF in recent statements argues that China’s economy is entering a “new normal” of slower but more “stable” growth. The IMF also has announced that the recent shock of the falling yuan to global markets actually makes the currency MORE viable for inclusion in the Special Drawing Rights global currency basket, a decision that is supposed to be finalized by November (though a year long extension has been recommended by the IMF before approval). Expect that economic news will be focused nonstop on China for the rest of the year, perhaps leading to the perpetuation of the false East/West paradigm and the idea that Americans should blame China for the overall financial crisis rather than the global bankers who engineered the mess. In the meantime, top globalists will continue to remain "neutral", presenting themselves as peacemakers and problem solvers arguing that the crash is "no one's fault", that over-complexity is the danger, and that interconnected economies must be simplified down to a single global currency and single global authority. U.S. Economy Feeling Effects The Federal Reserve push for a rate hike will likely be determined before 2015 is over. Talk of a September increase in interest rates may be a ploy, and a last-minute decision to delay could be on the table. This tactic of edge-of-the-seat meetings and surprise delays was used during the QE taper scenario, which threw a lot of analysts off their guard and caused many to believe that a taper would never happen. Well, it did happen, just as a rate hike will happen, only slightly later than mainstream analysts expect. If a delay occurs, it will be short-lived, triggering a dead cat bounce in stocks, with rates increasing before December as dismal retail sales become undeniable leading into the Christmas season. It is important to remember that the Fed's job is to DERAIL the U.S. economy, NOT protect it. In the meantime, the IMF’s SDR conference continues, with the inclusion of the yuan now widely considered a threat to the dollar’s world-reserve status. The mainstream media are now preparing the American people (or at least those who are paying any attention) for the coming loss of world-reserve status. The propaganda aims to paint the dollar’s reserve position as a bad thing. The MSM argue that loss of reserve status could actually help the U.S. economy get back on track and that a global harmonization of sovereign currencies will be a boost to our fiscal outlook. This is clearly an attempt to inoculate the public against any concern over the eventual crash of dollar value. Oil Price Panic Oil prices will continue to deflate, and the after-effects will be difficult to gauge. With John Kerrypublicly warning that the failure of an Iran deal (including the lucrative oil export deals that would be included) could lead to the loss of the dollar’s world-reserve status, I am not very optimistic about the future prospects of energy markets. Kerry claims that a failed Iran agreement would put the U.S. at odds with allies who brokered the deal, but this is not the whole story. What is really taking place is an attempt by Kerry to distract the public away from the real reasons for the future fall of the dollar, including the rise of the SDR and the likelihood that Saudi Arabia will soon decouple from the dollar as the solitary purchasing mechanism for their oil (Saudi Arabia is surprisingly one of the main supporters of an Iran deal). It is perhaps possible that a collapse of the Iran agreement could be used as an excuse for a loss of dollar reserve status that was going to happen anyway. Events Moving Faster Economic news is moving extremely fast this year, and it will only become more frenetic as we close in on 2016. The general consensus among alternative economic investigators seems to be that 2015 will be the year for trigger events and dead fantasies. In my six part series entitled'One Last Look At The Real Economy Before It Implodes' I essentially agree with this timetable. If 2014 was the new 2007 with all its immediate warning signs, then 2015 is the new 2008 with all the chaos and broken paradigms. @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@ 위안 투기꾼은 위안에서 그리고 금으로 이동하고 있습니까?제이 테일러 - 링크 - 나에게 Mongolio에 큰 볼리비아 실버 광산 프로젝트와 석탄 프로젝트를 인수 $ 100 백만 이상 상승 존 리, 예언 개발 공사 예언의 집행 위원장으로 중국의 평가 절하의 분석을 보냈습니다. 그는 중국에 상당한 시간을 보낸다. "생각할 필요도없는"중 하나가 "빌려"지난 몇 년 동안 거래 짧은에가, 또는 한 달러와 엔 약간의 비용을 수행하고 위안에 진행을 투자한다. 위안은 2006 년부터 달러 대 값에 올라가고 있었다 그러나 위안화를 평가 절하 시작하는 중국의 움직임은 투기가 긴장하라는되는 것은 피아트 통화 "차익 거래"입니다 대량 엉 무역을 실시하고 있습니다. 요한은 위안이 평가 절하 된 이유의 다양한 가능성을 통과하고 올해 상반기 동안 아래로 $ 400 억원이다 대규모 자본 유출과 외환 보유액에서 비롯 결론 지었다. 그 많은 양의 홍콩, 대만, 싱가포르로 이동했습니다. 그는 자본의 큰 덩어리의 소유자가 달러와 유로의 피곤한만큼이 흐름이 금으로 이동하고 있음을 시사한다. C의 히나과 인도는 세계 최대의 금 소비자의 두 가지이다. 당연히, 금 가격은 인민폐가 평가 절하 금의 감소 중국어 구매력을 부여 할 때 내려 갔다한다. 아주 그러나 반대로 금 가격은 인민폐 평가 절하 다음과 같은 다섯 가지 연속 거래일 동안 올라 갔다. 이유? 위안화 투기 가능성이 황금으로 위안 밖으로 이동하고 있습니까? 위안의 투자 가능성이 미국 달러에 대한 대안과 첫번째 장소에있는 유로를 추구하고 이것은 완전히 설득력이 될 수 있습니다. 상품 통화는 세계 경제의 둔화 주어진 매력이 남아 있었다. 금 시장은 연간 금 생산량은 약 US $ 160 억원, 지상 골드 주식 위의 총 모든 모양과 형태로, 약 $ 8 조원 한도로, 작습니다. 금에 대한 실제 수요가 조금이라도 증가는 금의 가격에 큰 영향을 미칠 수 있습니다. Are Yuan Speculators Moving Out of Yuan And Into Gold?Jay Taylor – LINK – sent me this analysis of China’s devaluation by John Lee, Executive Chairman of Prophecy Development Corp. Prophecy raised over $100 million to acquire a large silver mining project in Bolivia and coal projects in Mongolio. He spends a substantial amount of time in China. One of the “no-brainer” carry trades over the past couple years has been to short, or “borrow,” dollars and yen a very little cost and invest the proceeds in yuan. The yuan had been going up in value vs. the dollar since 2006. But China’s move to begin devaluing the yuan is prompting speculators to unwind the is fiat currency “arbitrage” carry trade en mass. John goes through the various possibilities of why the Yuan was devalued and concludes it stemmed from massive capital outflows and foreign exchange reserves which are down by $400 billion during the first half of this year. A large amount of that has moved to Hong Kong, Taiwan and Singapore. He is suggesting that this flow is moving toward gold as owners of large chunks of capital are tiring of dollars and euros. China and India are two of the world’s largest gold consumers. Naturally, gold prices should have gone down when the RMB was devalued, given the reduced Chinese purchasing power for gold. Quite to the contrary however, gold prices went up during five straight trading days following the RMB devaluation. The reason? Are RMB speculators possibly moving out of RMB into gold? This could be entirely plausible as RMB investors were likely seeking an alternative to the US dollar and the euro in the first place. Commodity currencies remained unattractive given the slowdown in the world’s economy. The gold market is small, with annual gold production amounting to approximately US$160 billion, and total above ground gold stocks amounting to approximately $8 trillion, in all shapes and forms. Even the slightest increase in physical demand for gold can have a profound impact on the price of gold. @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@ 세계 경제는 공식적으로 아래로 녹아

연준에서 월스트리트의 금융 및 관리 파티는 계속하고 싶은만큼, 그것은 마침내 중지에 관하여 본다. 구제 금융과 통화 팽창의 년 역사에서 가장 팽창과 인공의 경제 붐의 하나 만들었습니다, 지금은이 세계 경제의 거품이 기분을 가라 앉히는 것 같습니다. 우리가 말하는 전반적으로 시장이 폭락하고, 가정으로 "프린지"분석가들은 2008 예측 된 금융 사고는 우리에게 마지막이다. 지금 다운 무슨 일이 일어나고 있는지를 살펴 보자.

마지막 하나는 아주 말하고있다. 세계 경제가 다양한 상품의 값을 기준으로 나쁜 모양에있을 때 당신은 항상 알 수 있습니다. 그것이 유형의 상품이 생산되고 얼마나 많은 실제 알 수 있기 때문에 그것은 경제에 대한 가장 강력한 지표 중 하나입니다. 흥미롭게도,이 상품의 대부분은 우리가 2009 년 있었던 가정 회복을 통해 값에 떨어지는왔다. 지금 잘하고있는 유일한 상품은 6 주 최고치를 기록, 그냥 최선 주를했다 금이며,지난 1 월부터 . 금을 보유하고있는 안전한 피난처 상태를 감안할 때, 지금 미국 달러와 세계 경제에서 그 자신감 분명, 천천히 미끄러됩니다. 손이 모든 정보와 함께, 우리가 마침내 우리는 우리가 최근 6 년 동안 진정한 회복에 있었던 것으로 생각 2008 년 사람의 인내 충돌의 같은 종류를 목격 할 수 있음을 부인하기 어려운 것이었다 어리석은. 그러나 세계 시장은 단순히 다시 지난 몇 주 동안 발생한 것과 반송됩니다 생각 사람, 정말 미친 짓이야. The Global Economy Is Officially Melting Down

As much as the financiers on Wall Street and the officials at the Fed would like the party to keep going, it looks it’s finally about to stop. Years of bailouts and monetary expansion have created one of the most inflated and artificial economic booms in history, and now it appears that this global economic bubble is deflating. Markets across the board are melting down as we speak, and the financial crash that supposedly “fringe” analysts have been predicting since 2008, is finally upon us. Take a look at what’s going down right now.

That last one is very telling. You can always tell when the global economy is in bad shape based on the value of various commodities. It’s one of the strongest indicators for an economy, since it reveals how many real, tangible goods are being produced. Curiously, many of these commodities have been falling in value throughout the supposed recovery that we’ve been in since 2009. The only commodity that is doing well right now is gold, which has reached a six week high, and just had its best week since last January. Given the safe haven status that gold holds, it’s clear now that confidence in the US dollar and the global economy, is slowly slipping. With all of this information at hand, it would be hard to deny that we may be finally witnessing the same kind of crash that we endured in 2008. Anyone who thought that we’ve been in a genuine recovery for the past 6 years, was foolish. But anyone who thinks that global markets will simply bounce back from what has occurred over the past few weeks, is downright crazy. @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@ 그것은 충돌 포지션에 들어갈 시간인가? 어쩌면이 비행은 나 선식 급강하로 가지 않을 것이다; 아마도 그것은 단순히 연료의 부족. 전 세계 주식 시장 다이빙, 시급한 문제가 발생 : 그것은 충돌 포지션에 들어갈 시간이다? 경우에 당신은 충돌 위치로 가져 오는 방법을, 여기에 미리 알림의 깜빡 :

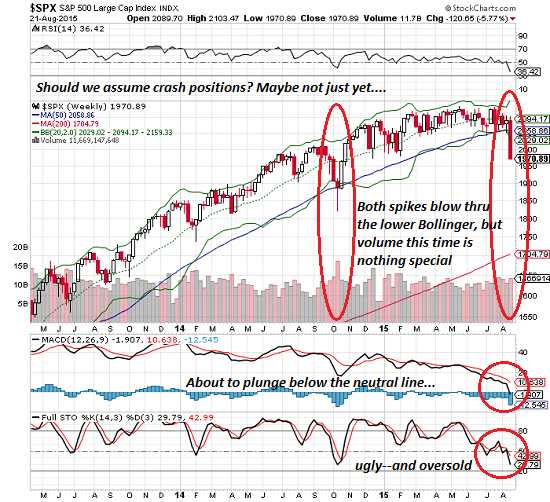

금요일에 다우에 현기증 500 포인트 하락 후, 우리는? 임팩트를 지탱해야 불시착의 전조 초기 침체로 이번 주에 기절을 볼 수있는 기본적이고 기술적 인 이유로 많이 있습니다. 우리 10 월 2014 년 다운 마지막 동등한 스파이크를 보면, 우리는 그렇게 확실하지 않다. 두 스파이크 (2015 2014년 10월 8 월)은 낮은 볼린저 밴드를 통해 박살하지만 지난 주 추의 부피는 2014 년 실신에 비해 특별한 것은 없었다. 그들은 거대한 볼륨을 동반하는 경우 큰 움직임은 좀 더 신빙성이있다.

이는 지난 10 월 다운 스파이크를 따라 어떤 날카로운 반등에 열린 문, 즉 나뭇잎. 풋 - 콜 비율 (CPC)은 두려움과 공포는 그때보다 지금 더 높은 수준에 있습니다 제안 년 10 월 2014 년 스파이크를 초과 실제로있다. 클릭당 비용 (CPC)의 날카로운 봉우리는 일반적으로 시장 바닥 신호.

그러나 시장은 반드시 더 높은 고음의 반환을 신호하지 않는, 크게 반등 경우에도 마찬가지입니다.새로운 최고 발생하지 않았다 만족의 극단적 인 신호 클릭당 비용 (CPC)의 최근 기온은; 시장 개월 동안 박스권하고있다. 이 불이 피곤 제안 - 가격이 다시 튀어 나올 경우에도 마찬가지입니다. SPX MACD가 마이너스를 통해 펀치를 위협 아래 중립 선에 그것의 방법을 일했다. 나쁜 일이 MACD가 중립 선 아래 비틀, 그 다음 감소가 작년의 스파이크 다운 - 스냅 백 패턴과 다를 수 있습니다 제안 할 때 발생하는 경향이있다. 그것은 충돌 위치로 할 시간인가? 그것은 준비를 상처 적이 있지만, 시장은 여기에 다른 2014년 10월 스냅 백을 끌어 경우, 시장은 활공 경로보다는 나 선식 급강하를 입력 할 수 있습니다. 연료 게이지에 눈을 유지합니다. 어쩌면이 비행은 나 선식 급강하로 가지 않을 것이다; 아마도 그것은 단순히 연료의 부족. Is It Time to Get into Crash Positions?Maybe this flight won't go into a tailspin; perhaps it simply runs out of fuel. With stock markets diving around the globe, a pressing question arises: is it time to get into Crash Positions? In case you forgot how to get into Crash Positions, here's a reminder:

After a dizzying 500+ point drop in the Dow on Friday, should we brace for impact? There are plenty of fundamental and technical reasons to view the swoon this week as the initial downturn that presages a crash landing. But if we look at the last equivalent spike down in October 2014, we're not so sure. Both spikes (October 2014 and August 2015) smashed through the lower Bollinger band, but the volume in last week's plummet was nothing special compared to the 2014 swoon. Big moves have a bit more credence if they're accompanied by massive volume.

This leaves the door open to a sharp rebound, i.e. what followed the spike down last October. The Put-Call Ratio (CPC) has actually exceeded the spike of October 2014, suggesting fear and panic are at higher levels now than back then. Sharp peaks in the CPC typically signal market bottoms.

But even if the market rebounds sharply, that doesn't necessarily signal the return of higher highs. Recent lows in the CPC signaling extremes of complacency did not result in new highs; the market has been range-bound for months. This suggests the Bull is tiring--even if price pops back up. The SPX MACD has worked its way down to the neutral line, threatening to punch through to negative territory. Bad things tend to happen when MACD stumbles below the neutral line, and that suggests the next decline might be different from the spike-down-snapback pattern of last year. Is it time to get into Crash Positions? It never hurts to be prepared, but if the market pulls another October 2014 snapback here, the market could enter a glide path rather than a tailspin. Keep an eye on the fuel gauges. Maybe this flight won't go into a tailspin; perhaps it simply runs out of fuel. |