퍼펙트 스톰 : 에픽 경제 붕괴에 대한 대비하세요

앞으로 몇 달 동안, 나는 우리가 2007 년 서브 프라임 모기지 붕괴의 6 배 이상 크기 경제 붕괴를 볼 수 있으리라 생각합니다.

상황은 내가 그것을 내가 장기 자본 관리 (LTCM)가 실패한 후 1998 년에 경험이 붕괴처럼 플레이 할 수 믿는지도한다.

이 시간은, 그러나, 투자자, 규제 당국이 준비가 떠나 몇 가지 중요한 차이가있을 것입니다.

사실, 지난 주, 나는 퍼펙트 스톰라는 라이브 정보 브리핑을 개최 : 1998 돌아 오는이 위험에 전략적 인텔리전스 독자들에게 경고.

하지만 브리핑 언급하지 않았다 어떤 두 개의 정보가 내 전망을 지원하는 데 사용되는 트리거했다.

나는 또한 나의 최고 투자 분석가 및 당신이 그들로부터 이익을 돕기 위해 식별 한 투자 아이디어를 공유하지 않았다. 우리는 예약 한 그 짐 Rickards '지능 트리거라는 나의 새로운 엘리트 서비스 중 하나의 베타 테스터.

난 당신이 먼저 순간에 그 격주 경고에 액세스 할 수 있지만 방법을 설명 제가이 시장 정보가이 위협을 확인 있다고 생각하는 이유에 대한 약간의 배경을 공유 할 수 있습니다 ...

시장 성과 가능성이 무엇인지 이해하기 위해, 우리는 우리가 알고있는 뭔가 시작하고 그것에서 추정.

국방 사회에서 군 지휘관은 마지막 전쟁을 싸우고 알려져있다. 그들은 다음의 충돌에 대비하여 그들의 이전 실패를 연구한다. 문제는 각 전쟁이 필연적으로 그들이 완전히 준비가있어하는 새로운 전술을 포함한다는 것입니다.

가장 유명한 사건은 1930 년대에 뒤로 보이는 마지노 선이었다. 차 세계 대전에서 독일의 급속한 발전에 대응하여, 프랑스는 독일이 다시 침입을 시도하는 경우 동원 할 시간을 벌어 자신의 국경에 콘크리트와 강철 요새과 장애물의 라인을 건설했다.

히틀러는 그것을이 공격에 중성 벨기에을 통해 프랑스를 침공하여 마지노 선은 무관했다. 프랑스는 준비가되었다. 몇 주 후, 독일군이 파리를 점령했다.

같은 실수는 금융권에서 이루어집니다. 금융 당국은 군 지휘관 다르지 않습니다. 그들은 마지막 전쟁을. 마지막 두 글로벌 원자로 붕괴는 1998 년과 2008 년, 지점의 경우입니다.

1998 년 금융 공황은 거의 글로벌 자본 시장을 파괴했다. 그것은 1997 년 6 월 태국에서 시작하고 인도네시아와 한국에 퍼졌다. 1998 년 여름, 러시아는 채무 불이행했고 그 통화가 붕괴. 그 결과 유동성 위기는 헤지 펀드 장기 자본 관리에 대규모 손실을 일으키는 원인이되었다.

내가 거기 때문에 손실에 대해 알고. LTCM의 수석 법률 고문, 나는 위기 8 월과 9의 높이 동안 모든 집행위원회 회의에서였다. 우리는 하루에 수억 달러의 손실을했다.두 달의 기간 동안 총 손실은 거의 4,000,000,000달러했다. 그러나 그것은 가장 위험한 부분이 아니었다.

우리의 손실은 우리가 가장 큰 월가의 은행과 우리의 책에 미친 파생 상품 거래 1 조 달러에 비해 사소한했다. LTCM이 실패한 경우, 거래의 그 조 달러는 돈을 지불하지 않았을과 월가의 은행들은 도미노처럼 떨어진 것이다. 글로벌 시장은 완전히 붕괴 것입니다.

나는 골드만 삭스, JP 모건과 씨티 은행을 포함하여 14의 가장 큰 은행의 지도자들과 구제 금융 협상을. 결국, 우리는 월스트리트에서 새로운 자본 40 억 달러를 가지고, 연방 준비 제도 이사회 (FRB)가 금리를 잘라 상황은 안정화. 그러나 일발, 뭔가 지금까지 반복하고 싶어 아무도이었다.

곧, 규제 당국이 헤지 펀드는 안전한 대출을 만들기 위해 밖으로 설정 때문에, 나를 위해 귀중한 교훈이었다. 그들은 더 밀접하게 자신의 헤지 펀드 노출을 모니터링하는 법적 문서를 개선하고 오픈 된 거래가의 성능을 확보하기 위해 더 많은 담보를 요구하는 은행을 주문했다.

규제 기관이 다음 위기를 방지 할 수 믿었다. 서브 프라임 모기지 - 2008 히트의 공포는, 그러나, 그들은 문제가되지 헤지 펀드에하지만 뭔가 새로운 것을 있었다 놀랐다합니다.모기지 시장의 붕괴는 신속하게 통제 돌다 다시 한 번 붕괴의 위기에 글로벌 자본 시장을 가져왔다.

2008 년 붕괴 한 후, 레귤레이터는 다시 마지막 전쟁을하기 위해 밖으로 설정합니다. 이것은 내가 예측있어 위기에 대한 설정입니다. 그들은 주택 대출이 이루어되기 전에 아래로 더 큰 지불, 더 나은 문서, 소득 증빙 서류, 재직 증명 및 높은 신용 점수를 요구함으로써 주택 담보 대출이 훨씬 안전했다. 그러나 다시 한 번, 오늘이 마지막 문제를 해결 완전히 다음을 무시하고 있습니다 조정기.

이미 우리의 레이더 화면에 다음 금융 붕괴는 헤지 펀드 또는 주택 모기지에서 제공되지 않습니다. 그것은 정크 본드, 특히 에너지 관련 및 신흥 시장 기업의 부채에서 올 것이다.

파이낸셜 타임스는 최근 탐사 및 개발을위한 2009-2014 발행 에너지 관련 기업 부채의 총량이 5조달러 이상이라고 추정했다. 한편, 국제 결제 은행은 최근 신흥 시장의 달러 표시 회사채의 총량이 9조달러 이상이라고 추정했다.

에너지 부문의 부채 때문에 유가의 붕괴의 질문이 제기되고있다. 그리고 신흥 시장의 부채로 인해 글로벌 성장 둔화, 글로벌 디플레이션, 그리고 강한 달러의 질문이 제기되고있다.

결과는 아마도 상환 또는 현재의 경제 상황에서 롤오버 할 수없는 기업의 부채 14조달러 더미입니다. 아니이 부채의 모든 기본 것이다, 그러나 많은 것이다.에너지 관련 부채의 대부분은 오일 배럴 범위 당 80 달러에 130달러 달러에 남아있을 것이라는 기대에 발행되었다. (I 바로 여기, 1 월 8 일보 응보의 역학을 설명했다.)

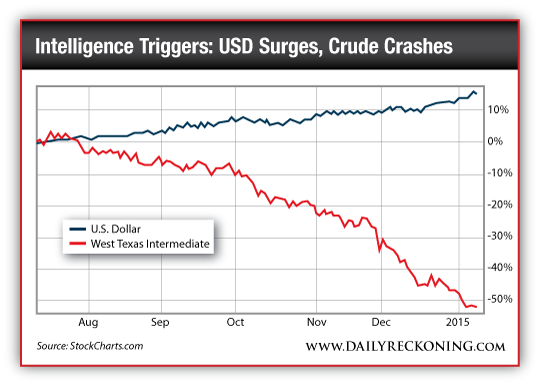

신흥 시장 채권의 대부분은 달러가 약 2,011 수준으로 남아있을 것 기대 발행했다. 대신 오일은 아래를 향하고 달러는 이러한 기대 그야하는 업입니다.이동은 신속하고 극적이었다.미국 달러 지수는 15 % 상승했다 지난 6 개월 동안, 오일은 52 % 추락했다.

보수적 인 가정 - - 기본 요금은 10 % 인 경우이 기업의 부채 대 실패는 세계는 2008 년 조정기에 1998 년 LTCM보다 훨씬 큰 부채 재앙과 모기지 시장에서 찾고있다 2007 년 서브 프라임 손실보다 여섯 배 이상이 될 것입니다 그들이 마지막 전쟁을 바쁜 되었기 때문에 이에 대한 준비가 전혀 안됩니다.

투자자를위한 좋은 소식이 큰 실수 하룻밤 일어나지 않을 것입니다. 그것은 밖으로 재생 년이 걸릴 것입니다. 1998년 9월의 패닉이 기준에 생방송 CNBC 해설자 짐 크레이머는 비명을 때, "그들은 아무것도 몰라!"2008 년 9 월 공포는 2007 년 8 월 전년 시작, 1997 년 6 월 태국, 전년 시작연방 준비 제도 이사회 (FRB)에.

이 새로운 정크 부채 대 실패는 2014 년 여름에 시작했지만 2016 이상까지 절정에 도달하지 않습니다. 어두운 전망과 심지어 기업과 국가는 종종 실제로 기본 전에 잠시 동안 지불을 손에 충분한 현금을 가지고있다. 한편, 당신은 이익을 수 있습니다.

채권 디폴트는 아직 일어나지 않았지만, 우리의 지능 트리거는 이미 유가 하락과 달러 강세의 형태로 볼 수 있습니다. 정보 분석에서, 우리는 일어날 재해를 기다리지 않습니다. 우리는 "표시 및 경고를"우리가 부르는 오늘날의 정보,보고 미래를 볼 수 이러한 역 확률로 추론 기술을 사용합니다.

강한 달러는 디플레이션이다. 이는 유가 가능성이 낮게 유지 것을 의미합니다. 이 에너지 부문 부채의 대부분은 돈을 지불 할 수 없으며 기본 의미합니다. 기본값은 아직 일어나지하지 않은,하지만 당신은 그들이 오는 것을 볼 수 있습니다. 이 당신이 정크 본드에서 오는 붕괴 이익을 할 수있는 기회는 아직이지만, 행동 할 수있는 시간은 지금이다.

감사합니다,

A Perfect Storm: Brace Yourself for an Epic Economic Meltdown

Over the coming months, I believe we could see an economic meltdown at least six times the size of the 2007 subprime mortgage meltdown.

Circumstances lead me to believe it could play out like the meltdown I experienced in 1998 after Long-Term Capital Management (LTCM) failed.

This time, however, there will be several crucial differences that will leave investors and regulators unprepared.

In fact, last week, I held a live intelligence briefing called The Perfect Storm: A 1998 Redux to alert Strategic Intelligence readers to the dangers.

But what I didn’t mention during the briefing were the two intelligence triggers I used to support my outlook.

I also didn’t share the investment idea that my top investment analyst and I have identified to help you profit from them. We’ve reserved that for the beta testers of one of my new elite services called Jim Rickards’ Intelligence Triggers.

I’ll explain how you can access those bi-weekly alerts in a moment, but first, let me share a little background about why I believe market intelligence confirms this threat…

To understand what market outcome is likely, we start with something we know and extrapolate from it.

In the national defense community, military commanders are known for fighting the last war. They study their prior failures in preparation for the next conflict. The problem is that each war inevitably involves new tactics for which they’re completely unprepared.

The most famous case was the backward-looking Maginot Line in the 1930s. In response to Germany’s rapid advances in WWI, France built a line of concrete and steel fortifications and obstacles on their border to buy time to mobilize if Germany tried to invade again.

Hitler made the Maginot Line irrelevant by outflanking it and invading France through neutral Belgium. The French were unprepared. A few weeks later, German forces occupied Paris.

The same mistake is made in financial circles. Financial regulators are no different than military commanders. They fight the last war. The last two global meltdowns, in 1998 and 2008, are cases in point.

In 1998, a financial panic almost destroyed global capital markets. It started in Thailand in June 1997 and then spread to Indonesia and Korea. By the summer of 1998, Russia had defaulted on its debt and its currency collapsed. The resulting liquidity crisis caused massive losses at hedge fund Long-Term Capital Management.

I know about the losses because I was there. As LTCM’s lead counsel, I was at every executive committee meeting during the height of the crisis that August and September. We were losing hundreds of millions of dollars per day. Total losses over the two-month span were almost $4 billion. But that wasn’t the most dangerous part.

Our losses were trivial compared with to the $1 trillion of derivatives trades we had on our books with the biggest Wall Street banks. If LTCM failed, those trillion dollars of trades would not have paid off and the Wall Street banks would have fallen like dominoes. Global markets would have completely collapsed.

I negotiated a bailout with the leaders of the 14 biggest banks including Goldman Sachs, JPMorgan and Citibank. Eventually, we got $4 billion of new capital from Wall Street, the Federal Reserve cut interest rates and the situation stabilized. But it was a close call, something no one ever wanted to repeat.

It was a valuable lesson for me, because soon after, regulators set out to make hedge fund lending safer. They ordered banks to monitor their hedge fund exposures more closely, improve their legal documentation and require more collateral to secure the performance on open trades.

Regulators believed this would prevent the next crisis. When the panic of 2008 hit, however, they were surprised that problems were not in hedge funds but in something new — subprime mortgages. The mortgage market collapse quickly spun out of control and once again brought global capital markets to the brink of collapse.

After the 2008 debacle, regulators again set out to fight the last war. This is the setup for the crisis I’m forecasting. They made mortgage lending much safer by requiring larger down payments, better documentation, proof of income, proof of employment and higher credit scores before a home loan could be made. But once again, regulators today are fixing the last problem and totally ignoring the next one.

The next financial collapse, already on our radar screen, will not come from hedge funds or home mortgages. It will come from junk bonds, especially energy-related and emerging-market corporate debt.

The Financial Times recently estimated that the total amount of energy-related corporate debt issued from 2009-2014 for exploration and development is over $5 trillion. Meanwhile, the Bank for International Settlements recently estimated that the total amount of emerging-market dollar-denominated corporate debt is over $9 trillion.

Energy-sector debt has been called into question because of the collapse of oil prices. And emerging markets debt has been called into question because of a global growth slowdown, global deflation, and the strong dollar.

The result is a $14 trillion pile of corporate debt that cannot possibly be repaid or rolled over under current economic conditions. Not all of this debt will default, but a lot of it will. Most of the energy related debt was issued in the expectation that oil would remain in the $80 to $130 dollar per barrel range. (I explained the dynamics in January 8th’s Daily Reckoning, right here.)

Most of the emerging markets debt was issued with the expectation that the dollar would remain at its weak 2011 levels. Instead oil is down, and the dollar is up, which capsizes these expectations. The moves have been swift and dramatic. Over the past six months, oil has crashed 52%, while the U.S. Dollar Index rose 15%.

If default rates are only 10% — a conservative assumption — this corporate debt fiasco will be six times larger than the subprime losses in 2007. The world is looking at a debt catastrophe much larger than LTCM in 1998 and the mortgage market in 2008. Regulators are completely unprepared for this because they have been busy fighting the last war.

The good news for investors is that this fiasco will not happen overnight. It will take a year or two to play out. The panic of September 1998 started a year earlier, in Thailand in June 1997. The panic of September 2008 also started a year earlier, in August 2007, when CNBC commentator Jim Cramer screamed, “They know nothing!!” on live television in reference to the Federal Reserve.

This new junk debt fiasco started in the summer of 2014 but will not reach its peak until 2016 or later. Even companies and countries with dim prospects often have enough cash on hand to make payments for a while before they actually default. In the meantime, you can profit.

The bond defaults have not happened yet, but our intelligence triggers are already visible in the form of lower oil prices and the strong dollar. In intelligence analysis, we don’t wait for disasters to happen. We look at today’s information, what we call “indications and warnings,” and use inferential techniques such as inverse probability to see the future.

The strong dollar is deflationary. This means oil prices will likely remain low. This means much of the energy-sector debt cannot be paid off and will default. The defaults have not happened yet, but you can see them coming. There is still an opportunity for you to profit from the coming collapse in junk bonds, but the time to act is now.

Regards,

http://cafe.daum.net/yoonsangwon/M9HA/15000

|